Broad Price Discovery In A Deleveraging World

January 26th, 2026

What we are observing across markets is not a collection of isolated moves, but a broad repricing of assets against fiat currencies. This process reflects long-term debt-cycle deleveraging, where balance sheets are gradually repaired and capital is forced to re-evaluate relative value rather than nominal price levels.

In such environments, price discovery does not unfold smoothly. Long stretches of apparent calm are often interrupted by sharp, nonlinear adjustments as leverage is reduced, funding conditions shift, or relative valuations snap back into alignment. These moves can be sudden and dramatic, even though they are part of a much longer structural process.

Because fiat prices alone can obscure this dynamic, we focus on cross-asset relationships — how assets behave relative to one another — to better identify where repricing has already occurred and where pressure continues to build.

Rates & Liquidity: The Anchor Point

What we are paying attention to on the chart: The U.S. is reaching a decision point for credit markets. Upward momentum is starting to fade, and we’re monitoring for a potential pivot.

Recent rate behavior suggests U.S. credit conditions remain broadly stable, though momentum appears to be maturing. Yield-curve dynamics are approaching levels that historically warrant closer attention, particularly if they begin to roll over in a sustained way. A meaningful downturn would likely signal renewed recessionary pressure and accelerate deleveraging forces.

We are also monitoring the U.S.–Japan rate spread as a barometer of global funding stress. As this spread narrows, yen-funded carry trades become less attractive, increasing the risk of forced selling in U.S. assets. While much of the compression has already occurred, recent stabilization suggests near-term pressure may be easing — for now.

Why Rates and Liquidity come first:

The cost of capital defines risk tolerance, governs leverage, and ultimately determines how aggressively assets can be held on balance sheets.

Bottom Line

U.S. credit markets appear broadly stable, though rate signals are nearing levels that warrant closer monitoring.

Energy: Repricing the Physical Economy

What we are paying attention to on the chart: We are expecting eventual mean reversion on the gold-oil ratio. We are on the lookout for RSI and stochastic indicators to provide the first signal of pivot.

When measured against gold rather than USD, oil appears deeply compressed. Historically, during periods of macro stress and balance-sheet repair, energy tends to reassert itself as capital rotates away from financial leverage and toward scarce, productive inputs. These relationships rarely resolve through prolonged stagnation; instead, they tend to correct via repricing.

Current cross-asset ratios suggest energy has lagged materially behind both precious metals and equities, creating conditions consistent with future mean reversion. If broader deleveraging continues, energy prices are likely to adjust higher in nominal terms to restore long-run real relationships.

Why Energy Comes Next:

Energy is best understood not as a standalone trade, but as a foundational input that must ultimately preserve its relationship to other real assets.

Bottom Line

Energy remains under-repriced relative to other real assets, leaving it vulnerable to sharp upward adjustments during repricing phases.

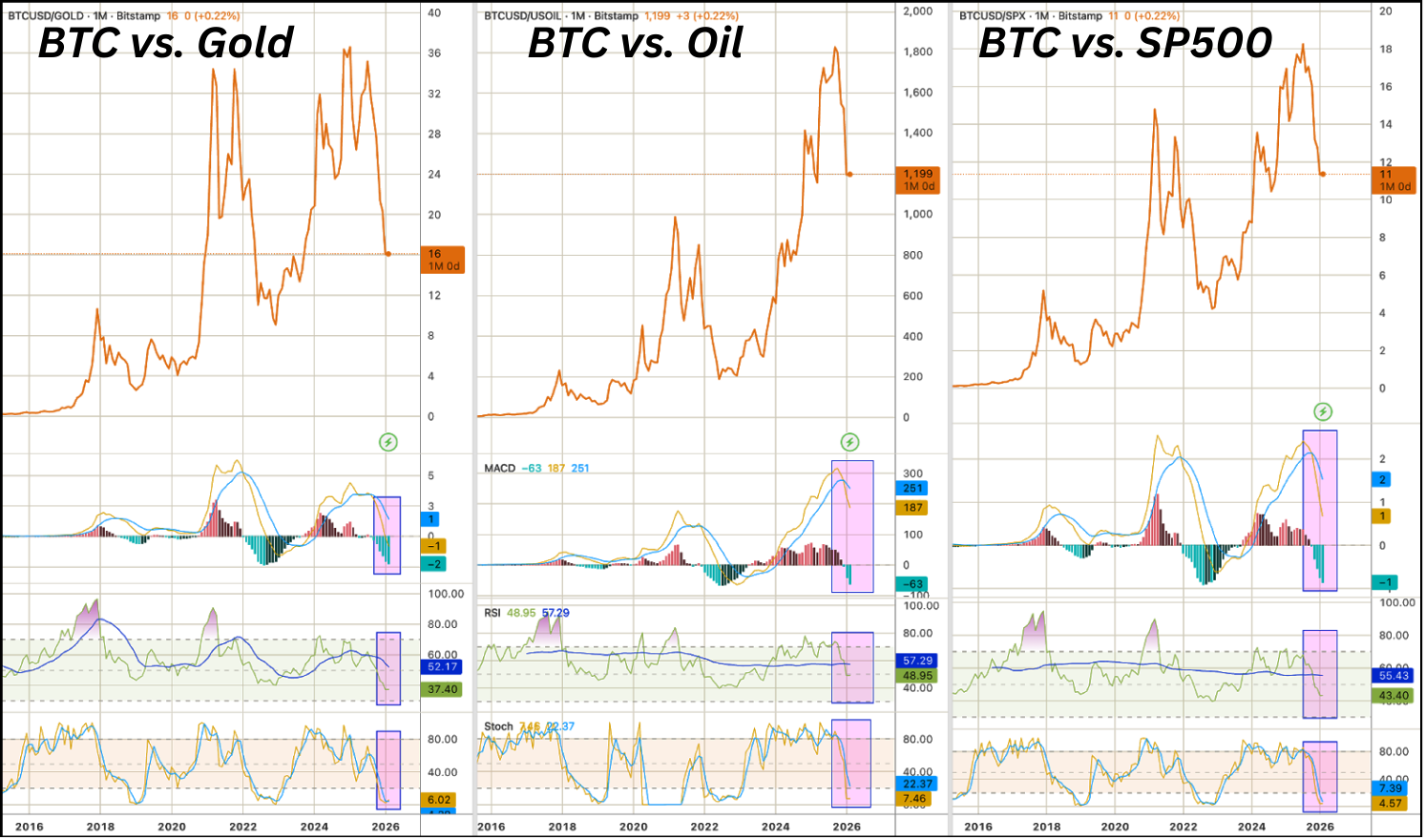

Bitcoin: The Cross-Asset Stress Lens

Bitcoin occupies a unique position at the intersection of liquidity, energy, and risk appetite. For that reason, we treat it as a stress lens rather than a standalone signal.

What we are paying attention to on the chart: The same momentum indicators of multiple cross-asset ratios are signaling that bitcoin might be close, though not yet quite all the way at the bottom of it’s downtrend. We are monitoring for downward momentum to finalize its cycle. The middle chart stands out, showing that Bitcoin may still have substantial repricing ahead relative to oil, particularly when contrasted with its positioning against gold or the S&P 500.

Market Structure Insight:

Relative comparisons show Bitcoin has retraced meaningfully against gold and equities, while remaining less compressed versus oil. This asymmetry implies that either Bitcoin weakens further relative to energy, or energy prices rise to rebalance the relationship — or some combination of both.

Importantly, viewed through a non-fiat lens, Bitcoin’s downside risk appears increasingly limited compared to earlier stages of the cycle. While volatility remains a feature, its relative positioning is becoming more consistent with an environment where real inputs are reasserting value and leverage is being worked off.

Bottom Line

Bitcoin supports the broader message of ongoing price discovery, while appearing increasingly attractive on a long-duration, relative-value basis.

Real Estate: Lagging, Not Broken

Real estate typically lags early-stage repricing in real assets, largely due to financing constraints and slower turnover. Gold often outperforms real estate during periods of uncertainty, but this divergence has historically resolved through real estate appreciation rather than sustained underperformance.

Current gold-to-real-estate ratios suggest that divergence may be nearing exhaustion. While real estate is unlikely to lead the next phase of repricing, relative valuations are becoming more constructive as financing conditions gradually adjust.

Defense Equities: Late-Cycle Expression of Risk

Defense equities tend to perform best once geopolitical risk is broadly acknowledged rather than merely anticipated. Recent outperformance reflects elevated uncertainty already priced into markets.

While structural demand remains intact, relative valuations suggest risk-adjusted returns are becoming less compelling. At this stage, defense appears more indicative of risk already recognized than a source of asymmetric opportunity.

Closing Thoughts:

Taken together, these signals point to a market environment defined by ongoing balance-sheet repair and broad price discovery. Assets are increasingly communicating through their relationships with one another rather than through headline price moves alone.

This deleveraging process is likely to be long and uneven. Periods of stability can coexist with sudden, forceful repricing as leverage is reduced and relative value is re-established. Understanding where those pressures are building, before they surface in nominal prices, is essential for navigating the cycle ahead.

Look out for next week’s newsletter for further insight into the forces shaping today’s markets.