From Signals to Confirmation

March 22nd, 2026

Markets are increasingly favoring liquidity itself, while early stress begins to reach corporate credit.

Risk in markets is often described in terms of asset prices — equities, bonds, commodities.

But in practice, risk is not defined by assets alone. It is defined by how those assets relate to liabilities.

For any investor — whether an individual, a corporation, or a financial institution — the true question is not simply “what is this asset worth,” but:

“Will this asset reliably meet the obligations I have coming due?”

In periods of uncertainty, that question becomes more important.

And the answer often leads to a shift in behavior.

Instead of simply rotating into traditionally “defensive” assets, markets can begin to favor liquidity itself — assets that can directly meet liabilities without conversion risk.

Over the past several weeks we have been observing a set of signals forming across markets.

This week, those signals are no longer isolated — they are beginning to confirm.

Three developments stand out:

Risk appetite continues to compress

Credit conditions are beginning to respond

Capital behavior is shifting toward liquidity preference

Markets Are Choosing Liquidity

The shift we are observing did not begin with a move into liquidity.

Earlier in the process, capital rotated toward traditional defensive assets — most notably gold — as markets began to price in higher uncertainty.

That phase reflected a classic risk-off response.

What we are observing now is a continuation of that process — but with a meaningful shift in emphasis.

Equity markets have continued to weaken, with both the S&P 500 and Nasdaq reaching recent lows.

Market breadth has deteriorated further, with a declining share of stocks holding above long-term averages.

Volatility remains elevated, not as a sudden spike, but as a persistent feature of the environment.

At the same time, bond market volatility continues to rise, suggesting that uncertainty at the macro level remains unresolved.

Gold — one of the primary defensive assets — has retraced meaningfully over the past couple of weeks.

This combination of risk assets and defense assets both selling off suggests that markets are no longer simply seeking defense.

They are increasingly seeking liquidity itself.

In practical terms, this reflects a shift toward assets that can directly meet obligations — rather than assets that must first be converted under uncertain conditions.

When uncertainty rises far enough, the question is no longer:

“Which asset will perform best?”

It becomes:

“Which position leaves me most flexible if conditions change?”

At the same time, fiscal dynamics are playing a more active role in the liquidity environment.

The Treasury General Account — effectively the government’s cash balance — is not just a passive indicator, but an active participant in the system.

When the Treasury builds its balance, it is effectively drawing liquidity out of the financial system.

In the last week, the Treasury has been absorbing liquidity rather than adding it.

In that sense, the Treasury itself is competing for liquidity alongside market participants.

In an environment where investors are already prioritizing flexibility and reserves, that additional demand for liquidity can reinforce the broader shift in behavior. The shift is not abrupt, and it is not absolute.

Markets rarely move cleanly from one regime to another. Instead, what we are observing is a gradual evolution —

market participants adjusting their behavior as underlying conditions change.

What began as a rotation into defensive assets is now developing into a broader preference for liquidity.

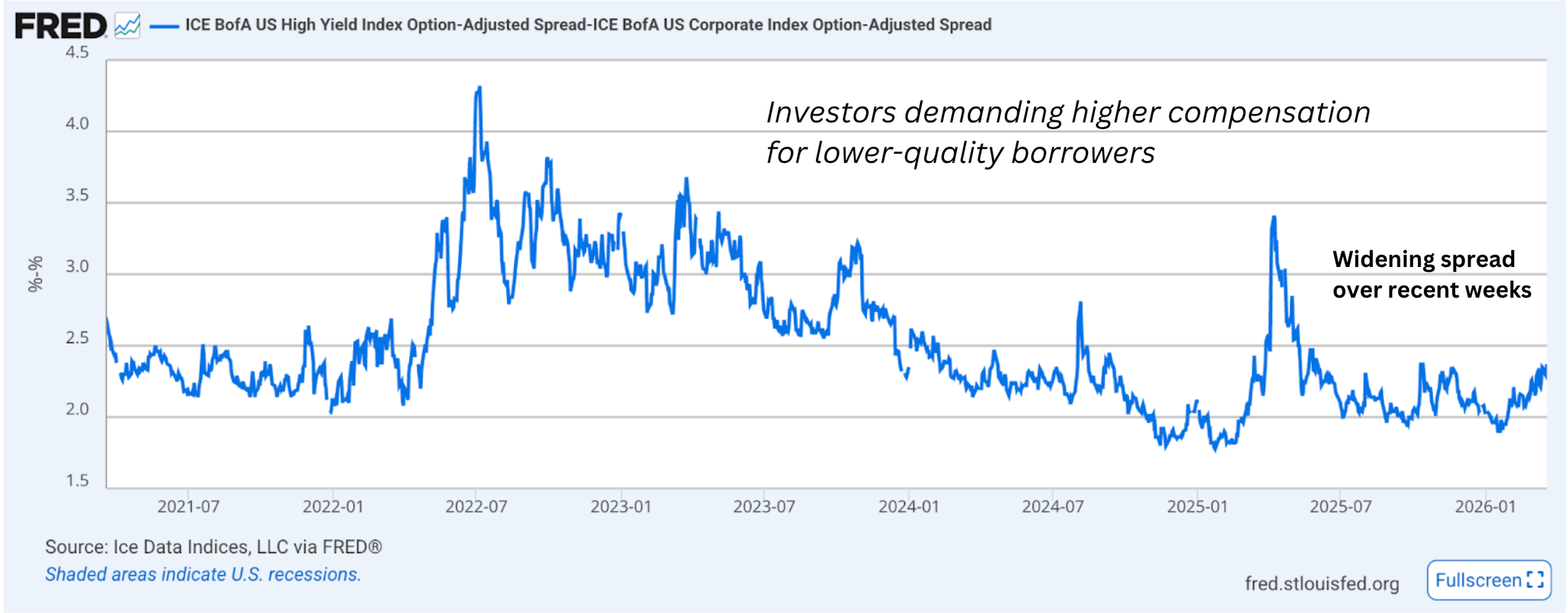

Credit Is Beginning to Confirm

If changes in risk appetite are the first signal, credit markets are often where those changes begin to confirm .

The spread between high-yield and investment-grade corporate bonds has continued to widen and now sits at its highest level in recent weeks.

The move remains gradual, but the consistency is notable.

The spread between high-yield and investment-grade debt continues to widen, signaling increasing selectivity in credit markets.

When this gap increases, it typically means investors are becoming more selective about the credit risk they are willing to take.

In other words, capital is beginning to differentiate more clearly between stronger and weaker balance sheets.

This is where market signals begin to move beyond pricing and into behavior.

When credit conditions tighten:

Investors rotate toward higher-quality debt

Lower-quality borrowers face higher financing costs

New issuance becomes more difficult or more expensive

For companies, this can translate into:

delayed capital investment

slower hiring decisions

more cautious expansion plans

What began as a shift in market sentiment is now beginning to touch corporate financing conditions.

This is the transition from signal to confirmation.

The Shift Is Not Local

The developments we are observing are not confined to a single market.

Emerging markets have declined meaningfully over the past several weeks, reaching their lowest levels in the current observation window.

At the same time, measures of Chinese credit activity have also weakened, pointing to a broader slowdown in global credit impulse.

These moves suggest that the shift we are observing is not isolated to U.S. equities or U.S. credit markets.

Instead, it reflects a broader, cross-market adjustment in how capital is being allocated.

The alignment across regions reinforces the idea that this is a coordinated repricing of risk — not a localized event.

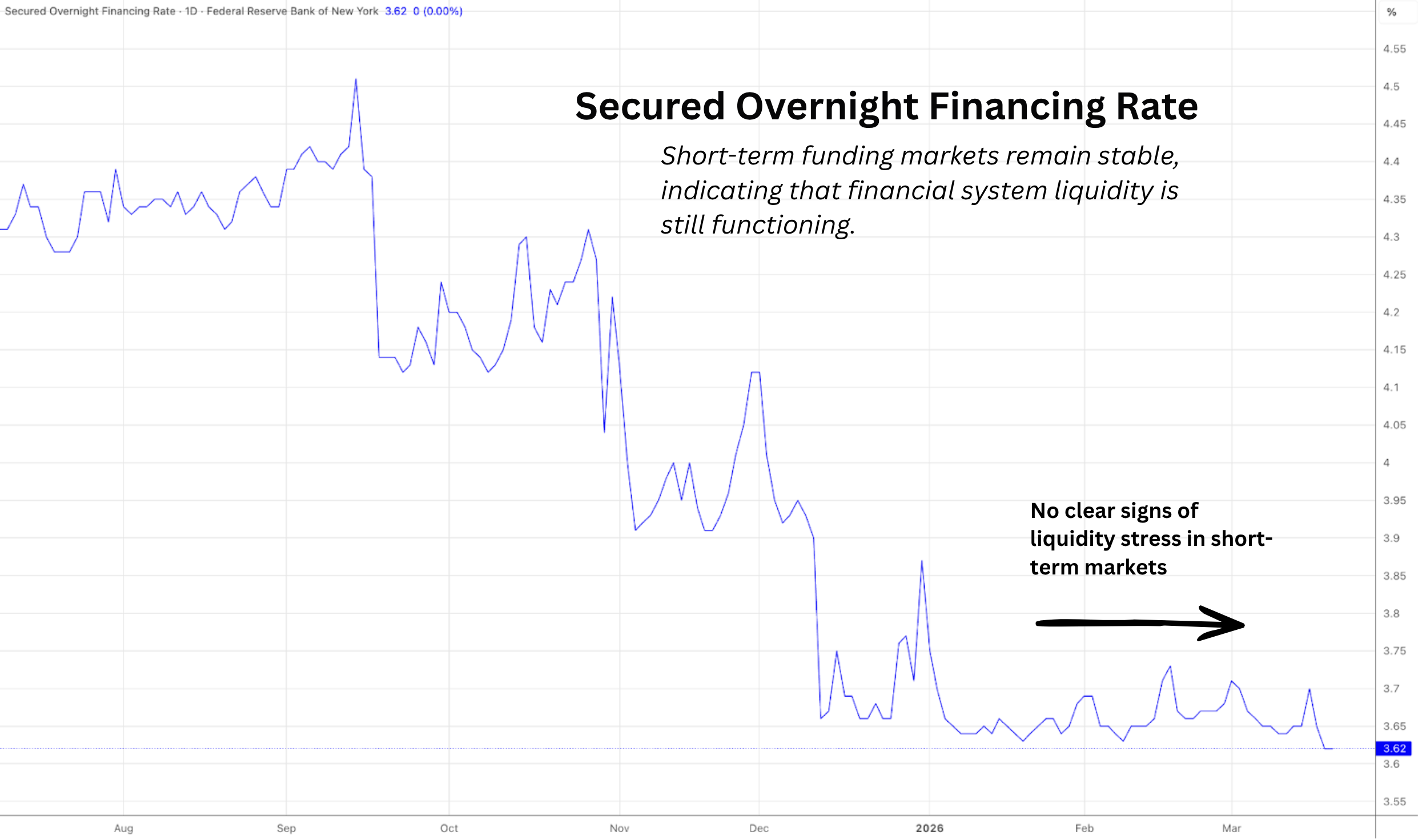

The System Is Absorbing It — For Now

Despite these developing pressures, the core of the financial system continues to function.

Short-term funding markets remain stable.

Key funding rates have not shown signs of stress.

Short term liquidity channels — the underlying plumbing of the system — remain intact for now.

Credit markets determine how expensive it is to borrow.

Funding markets determine whether the system can continue to operate smoothly.

At present, we are seeing pressure in the former — but not disruption in the latter.

That means:

no forced deleveraging

no liquidity freeze

no systemic break

At the same time, the accumulation of signals across volatility, credit, and global markets suggests that the system is absorbing a growing amount of pressure.

The system is holding —

but it is no longer as untested as it was just a few weeks ago.

What This Means Now

The most important development this week is not any single market move, but where those moves are beginning to show up.

What we are observing is the early stage of market dynamics beginning to move beyond asset prices and into corporate conditions.

As credit spreads widen:

financing becomes more expensive

investment decisions become more cautious

economic activity begins to adjust at the margin

This is how financial conditions transmit into the real economy — gradually, and often before it is visible in traditional economic data.

The shift taking place is subtle, but meaningful.

Markets are increasingly prioritizing liquidity even over traditional defensive assets,

and that shift is beginning to make its way into the real economy.

Look out for next week’s newsletter for further insight into the forces shaping today’s markets.