When Liquidity and Markets Begin to Move Together

March 30th 2026

Markets are already adjusting — while liquidity conditions are beginning to shift alongside them

There’s Something Worth Noting

There are moments where individual data points matter less than how they begin to interact.

Over the past several weeks, markets have already been adjusting.

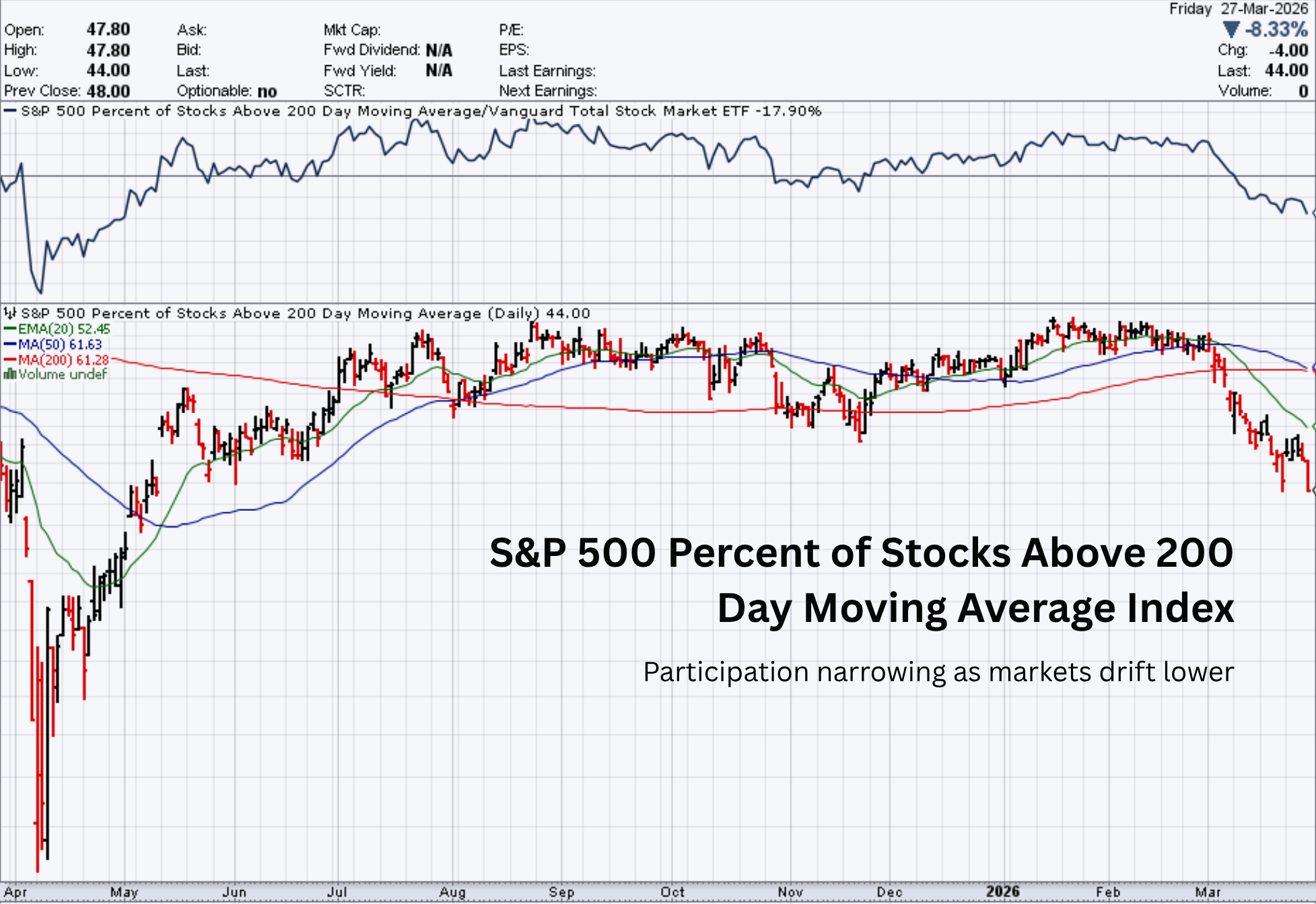

Equities have continued to drift lower, participation has narrowed, and credit spreads have begun to widen. None of these moves are extreme—but the direction has been consistent.

At the same time, another development has quietly re-emerged.

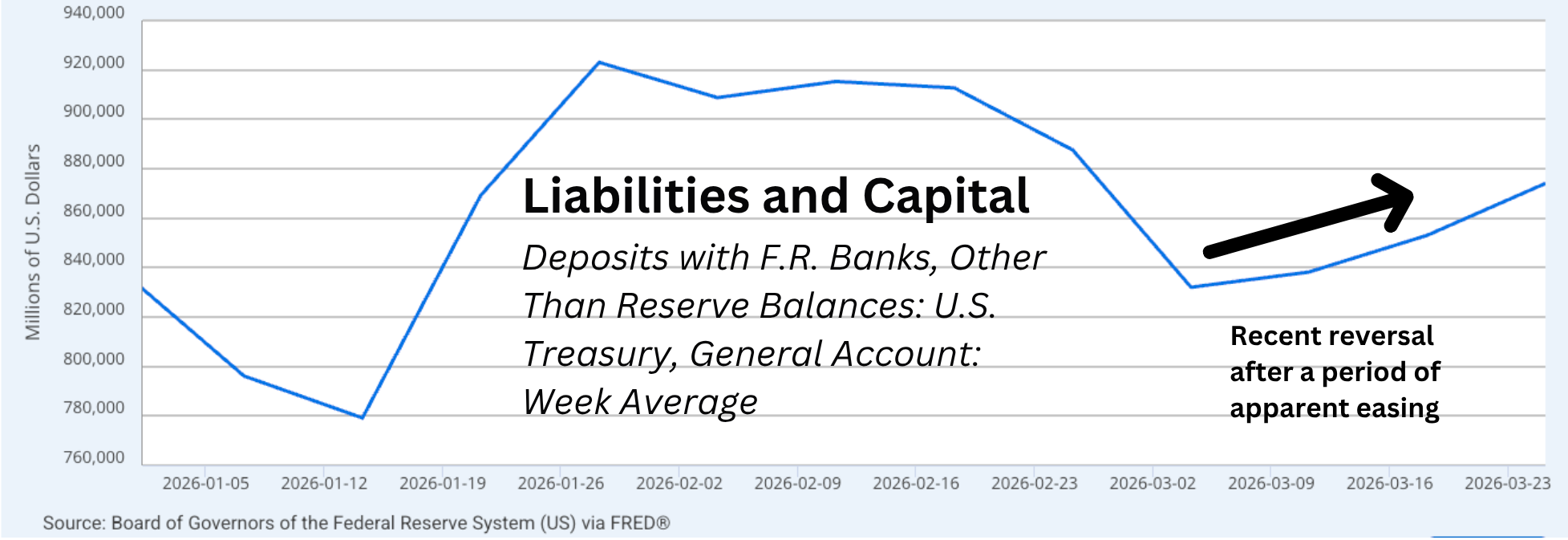

After appearing to stabilize—and even ease—the U.S. Treasury’s cash balance has now begun to rise again.

On its own, that might not stand out. But in the context of already-softening markets, it becomes more interesting.

And it leads us to a simple question:

If markets are already under some pressure, what happens if there’s simply less liquidity available to go around?

What We’re Actually Seeing

Let’s anchor this in the data.

The Treasury General Account (TGA)—effectively the government’s cash balance at the Federal Reserve—has now increased for three consecutive weeks, rising back toward recent highs.

Current level: ~$874B

Recent peak (8 weeks ago): ~$974B

A few weeks ago, the trajectory suggested liquidity might be easing back into the system. That direction has, at least for now, reversed.

At the same time:

Equities (S&P 500, Nasdaq) continue to trend lower

Market breadth continues to deteriorate

Credit spreads (High Yield vs Investment Grade) are widening

Emerging markets and China credit have rolled over

Individually, none of these are definitive.

Together, they suggest that markets are already adjusting to tighter conditions.

What the TGA Actually Does

To understand why this matters, we need to understand what the TGA represents.

The Treasury General Account is the pool of cash the U.S. government holds at the Federal Reserve.

When that balance rises, cash is effectively pulled out of the private financial system.

When it falls, that cash is released back into the system.

This is not a directional policy signal—it’s operational.

But mechanically, it influences how much liquidity is available across markets.

It’s less about intention, and more about where cash is sitting at a given moment in time.

Why This Moment Stands Out

What makes this moment notable is not the TGA in isolation—and not market weakness in isolation.

It’s the overlap.

Markets have already begun adjusting—gradually, but consistently.

At the same time, liquidity—at least at the margin—is no longer clearly easing.

These developments are occurring at the same time—and that overlap is worth paying attention to.

We are not seeing stress.

But we are beginning to see alignment across different layers of the system.

Exploring the Question

So we return to the question:

If markets are already under some pressure, what happens if there’s simply less liquidity available to go around?

Rather than jumping to conclusions, it’s more useful to think through how this dynamic works.

Markets Are Sensitive to Liquidity—Especially at the Margin

Markets are not driven by fundamentals alone—they are heavily influenced by the availability of capital.

When liquidity is abundant:

Risk is more easily absorbed

Volatility tends to compress

Credit flows more freely

When liquidity becomes more limited:

Markets become more sensitive

Positioning becomes more cautious

Buyers become more selective

This doesn’t create immediate stress—but it changes behavior.

Liquidity Doesn’t Need to Collapse to Matter

Even small shifts can:

Reduce excess cushion

Increase sensitivity to new information

Amplify existing trends

This becomes more relevant when markets are already in a fragile or adjusting state.

This Is About Interaction—Not Direction

It’s tempting to simplify:

“Liquidity down → markets down”

But that misses the point.

What matters is that markets and liquidity are now interacting, rather than moving independently.

That interaction is where insight lives.

The System Remains Stable

Despite all of this:

Funding markets are functioning

No signs of systemic stress

No breakdown in financial plumbing

The system itself remains stable.

And that’s an important anchor.

What This Means for Investors

Understanding this dynamic changes how we interpret the environment.

It’s no longer just about direction—it’s about conditions.

Right now:

Markets are adjusting

Liquidity is no longer clearly easing

Credit is beginning to reflect caution

But the system remains stable

That combination matters more than any single signal.

Closing Thought

Markets are already moving.

At the same time, liquidity conditions are beginning to shift at the margin.

Neither development alone defines the moment—but together, they begin to shape it.

For now, that interaction is simply something worth paying attention to.

Look out for next week’s newsletter for further insight into the forces shaping today’s markets.