A First Look at Bitcoin-Linked Credit

April 27th 2026

Why markets are beginning to build financial products around Bitcoin-heavy balance sheets

Something new is developing in financial markets.

For most of its history, Bitcoin has been understood in relatively simple terms. It is something you buy, hold, and, if needed, sell. It does not produce income. It does not generate cash flow. Its role has mostly been defined by what it is: a scarce digital asset.

But that framing is starting to expand.

A small but important group of companies is now treating Bitcoin not only as an asset to hold, but as something financial markets can build around. The clearest example is Strategy, formerly MicroStrategy, which has developed a growing capital structure around its Bitcoin-heavy balance sheet.

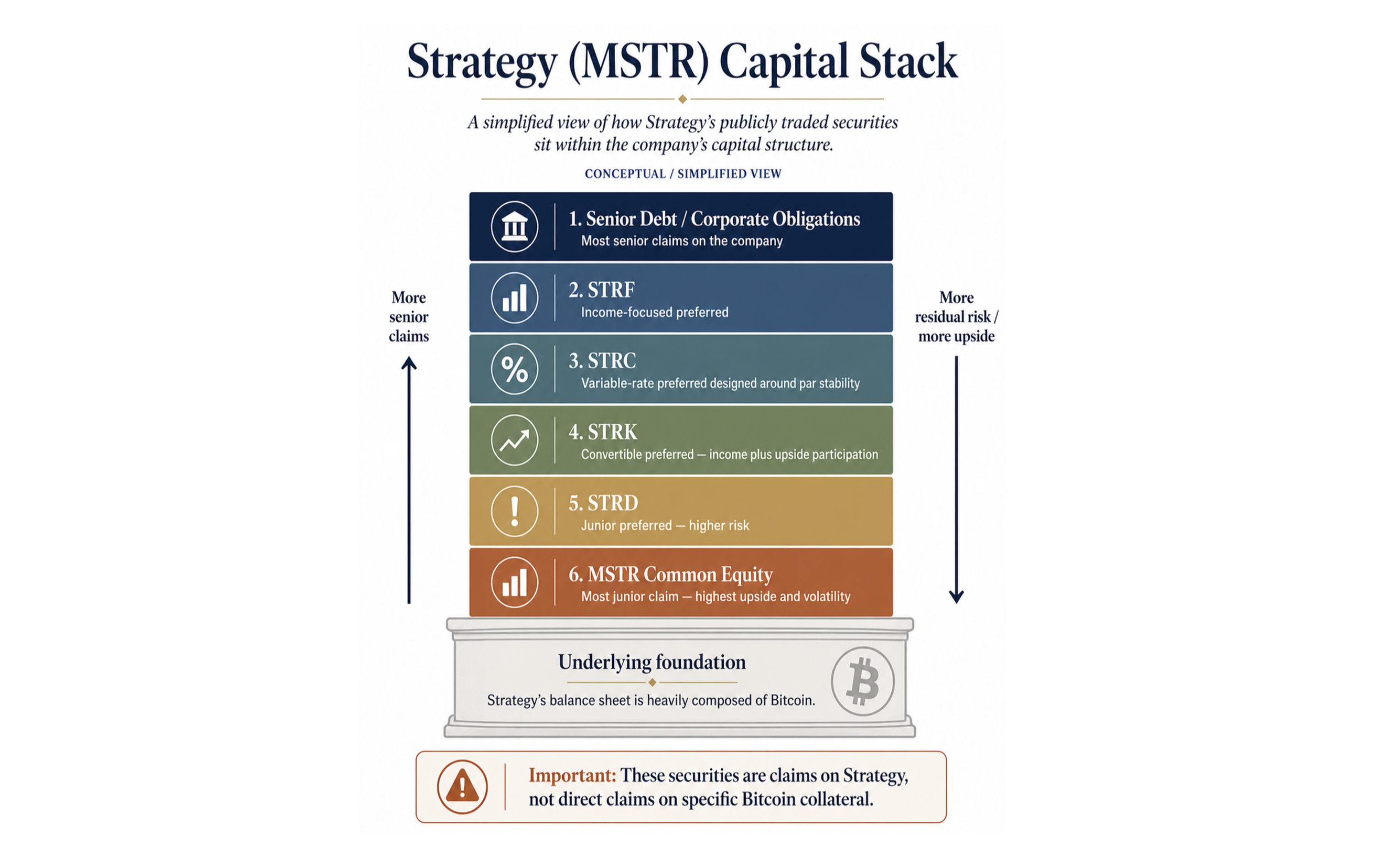

This does not mean these products are “Bitcoin-backed loans” in the legal sense. Strategy’s own materials state that its preferred securities are not collateralized by the company’s Bitcoin holdings and only have a preferred claim on the residual assets of the company. (Strategy)

That distinction matters.

These products are better understood as Bitcoin-linked credit products: securities issued by a company whose balance sheet is heavily tied to Bitcoin.

And that makes them worth understanding.

Why would a company do this?

Start with the basic problem.

If a company holds Bitcoin, selling provides liquidity but reduces exposure. Holding preserves exposure but produces no cash. Traditional finance has long solved this problem by allowing companies and investors to raise capital around assets rather than selling them outright.

Strategy is applying that logic to Bitcoin.

Instead of selling Bitcoin, the company issues securities, raises capital, and keeps its Bitcoin exposure intact. Strategy has described STRC as a variable-rate preferred stock designed to trade near a $100 stated amount, with dividends adjusted to support that objective. (Nasdaq)

In plain English:

The company is trying to turn Bitcoin from a passive treasury asset into a financing base.

That is the real story.

Not yield. Not hype. A financing base.

The preferred stack: four products, different roles

Strategy’s publicly traded preferred securities give investors different ways to take exposure to the same broad issuer and balance-sheet story.

They are not all the same product.

STRF sits closer to the senior income layer. STRC is designed as a variable-rate preferred aiming to remain near par. STRK includes convertibility and therefore more upside participation. STRD sits further out on the risk spectrum as the more junior preferred layer. Secondary explainers describe the four series as differing in seniority, dividend structure, and convertibility, with STRF generally senior and STRD more junior. (Backpack Learn)

The simple version:

STRF is for investors who prioritize income and relative seniority.

STRC is for investors focused on income with a product designed around price stability near par.

STRK is for investors who want income plus more upside participation through convertibility.

STRD is for investors willing to accept more risk within the preferred stack.

The key idea is that Strategy is not just issuing one instrument. It is building something closer to a capital stack around a Bitcoin-heavy balance sheet.

Different investors can choose different layers depending on what they want: income, stability, upside, or risk.

Why this is not simply a pyramid

At first glance, the structure can raise an obvious question.

If a company raises money, buys more Bitcoin, and then raises more money against a larger Bitcoin balance sheet, is that just a self-reinforcing loop?

It is a fair question.

But the cleaner answer is this:

Investors are not funding earlier investors. They are pricing risk around a company with a large Bitcoin-heavy balance sheet.

That does not make the structure risk-free. It does make it different from a pyramid dynamic.

There are real assets on the balance sheet. There are real market constraints. There are real dividend obligations. And there is no guarantee that capital markets will continue to accept new issuance on attractive terms.

That last point is important.

A structure like this only works while investors are willing to price the securities, buy the products, and trust the issuer’s balance sheet. If demand weakens, issuance becomes harder. If Bitcoin falls materially, balance-sheet confidence can weaken. If dividend obligations grow too large, the structure becomes more fragile.

So this is not magic.

It is capital markets engineering.

The mechanism: borrow around Bitcoin instead of selling it

The core mechanism is simple.

Strategy holds Bitcoin. It issues securities against the company. Investors buy those securities for income, stability, or upside participation. Strategy raises capital while preserving Bitcoin exposure.

That creates a new role for Bitcoin.

It is no longer just an asset sitting on the balance sheet.

It becomes part of how the company structures capital.

Why this matters: adoption looks like infrastructure

The importance of these products is not that they prove a bullish Bitcoin thesis.

They do not.

The importance is that they show financial markets beginning to build around Bitcoin.

That is typically what happens as an asset matures. Markets create wrappers, financing tools, derivatives, income products, hedging instruments, and structured exposures. The asset becomes less isolated. It becomes part of a broader financial system.

Bitcoin appears to be moving through a version of that process.

First, it was a speculative asset. Then it became a store-of-value candidate. Then it moved onto corporate balance sheets. Now, at least in early form, markets are building financing products around Bitcoin-heavy companies.

That is a development worth observing.

Not because it tells us where Bitcoin trades next week.

But because it shows how adoption can appear in market structure.

What could go wrong

The risks are real.

The first is legal and structural. These products are not directly collateralized by Bitcoin. Preferred holders rely on the company, not a segregated claim on specific BTC holdings. Strategy states this directly in its own preferred security materials. (Strategy)

The second risk is Bitcoin volatility. If Bitcoin falls materially, the balance sheet weakens, market confidence can decline, and new issuance may become more difficult.

The third risk is dividend burden. Preferred securities create obligations. Those obligations need to be serviced, and market reporting has highlighted investor focus on Strategy’s preferred dividend and debt servicing costs.

The fourth risk is complexity. These products may look like income instruments, but their behavior is tied to a company whose financial structure is heavily connected to Bitcoin.

That combination can be powerful.

It can also be misunderstood.

What to watch

The first thing to watch is whether issuance continues to grow. If more capital is raised through these structures, it suggests investors are willing to keep funding the model.

The second thing to watch is STRC.

STRC matters because it is designed to trade near a $100 stated amount, with a variable dividend mechanism intended to help maintain price stability. Strategy has specifically referenced STRC’s variable dividend mechanism and its role in maintaining price near the stated amount.

That makes STRC a useful pressure gauge.

If STRC remains stable near par, it suggests demand is strong enough for the structure to function as intended. If it breaks away from par for a sustained period, that may signal stress in investor demand, pricing, or confidence.

The third thing to watch is how these products behave during a sustained Bitcoin drawdown.

That is the real test.

The structure is easiest to understand when Bitcoin is stable or rising. The more important question is how it behaves when Bitcoin falls, capital markets tighten, or investor appetite weakens.

Final thoughts

Something new is forming.

Not in a way that requires immediate action.

And not in a way that offers easy conclusions.

But in a way that is worth understanding.

Companies are beginning to raise capital around Bitcoin-heavy balance sheets. Markets are creating different securities for different investor needs. And Bitcoin is slowly becoming something financial products can be built around.

That is what adoption often looks like.

Not just price movement.

Infrastructure.

And right now, we may be watching the early stages of that infrastructure being built.

Look out for next week’s newsletter for further insight into the forces shaping today’s markets.