Policy Posture Meets Structural Constraint

February 16th, 2026

This week we review how markets are navigating a growing tension between policy tone and economic reality.

A recent conservative tone from the future Federal Reserve chairman, Kevin Warsh, suggests policymakers may be slower to ease, even as economic softness becomes more visible. At the same time, global funding dynamics are tightening the room for maneuver.

The result is not a clear tightening cycle, nor a clean easing regime. It is something more complex: a constrained system where each adjustment carries external consequences.

Gold, more than any single policy speech or data release, appears to be revealing how this tension is resolving.

The Fed: Conservative Posture, Uncertain Path

“The Fed’s balance sheet is trillions larger than it needs to be. A smaller balance sheet could actually allow for lower interest rates.”

Structural Insight:

Recent comments from the incoming Fed leadership emphasize balance-sheet discipline and a preference for monetary orthodoxy.

This does not amount to an announced tightening campaign. Nor does it imply immediate quantitative tightening. What it does signal is caution — a reluctance to lean quickly toward accommodation.

That tone matters. The Fed is not clearly easing, but neither is it clearly tightening. The signal is conservative posture amid rising macro tension.

Why This Matters:

When central bank leadership emphasizes restraint, markets interpret that as a higher hurdle for accommodation. This shapes expectations and risk pricing — even if no policy change has occurred.

Bottom Line

The Fed’s conservative posture suggests policymakers may be slower to ease, even as economic softness becomes more visible.

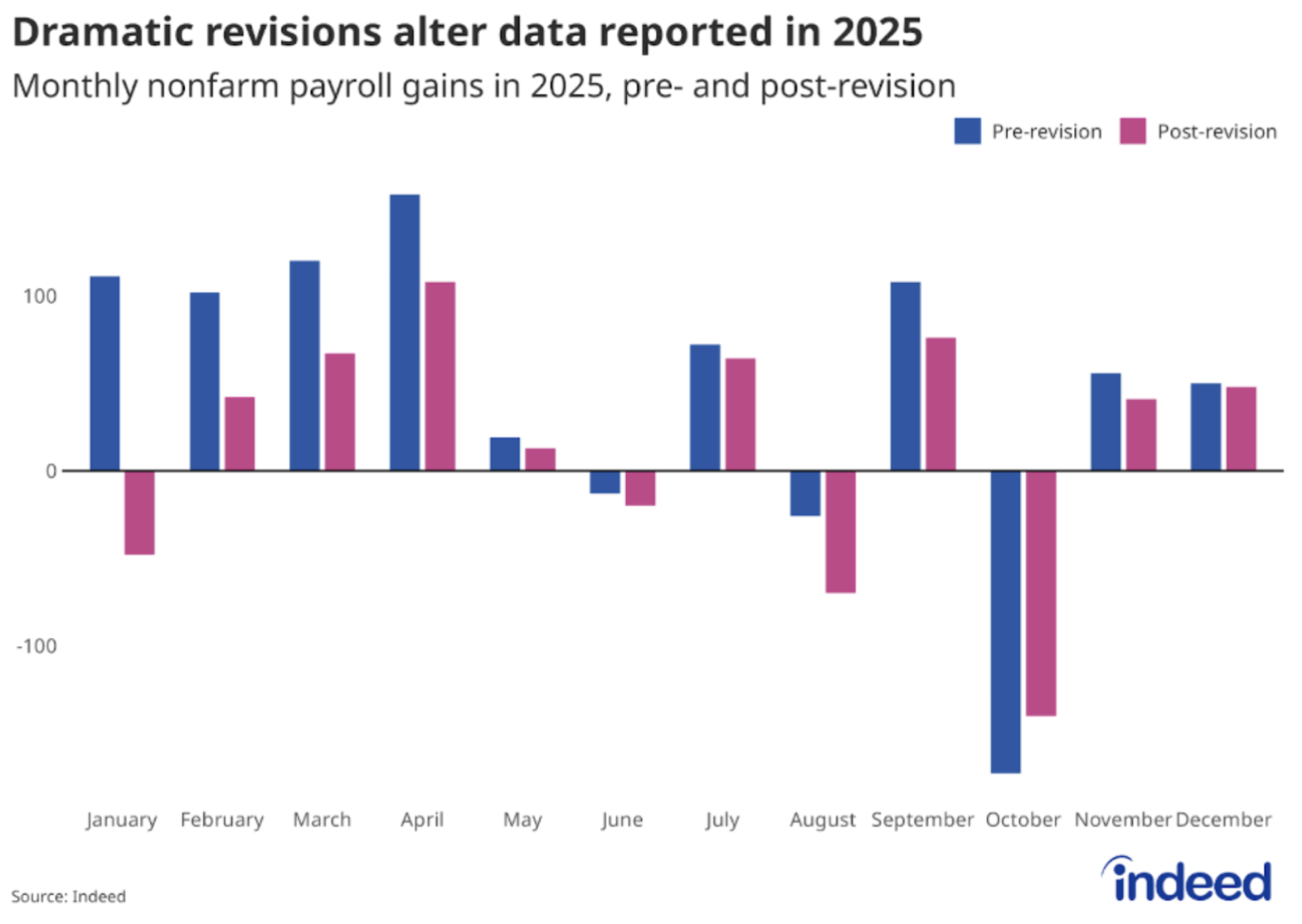

Labor Data: Softness Beneath the Surface

The labor picture has become less convincing.

A substantial downward revision to 2025 employment figures, along with falling inflation-adjusted entry-level wages, suggests that underlying conditions may be weaker than headline data previously implied.

This combination is important:

Slower job growth

Real wage compression

Weakening entry-level purchasing power

These are not signs of an overheating economy.

They are signs of strain.

Why This Matters:

Under normal conditions, weaker labor data would increase the probability of easing. But with policy tone cautious and global funding constraints tightening, accommodation is not straightforward.

Bottom Line

Labor data revisions and real wage compression point to a softer economy than popular belief.

The US–Japan Spread: A Global Constraint

If yields decline too quickly, yen carry trades unwind, potentially pressuring U.S. asset markets and complicating monetary adjustments.

Market Structure Insight:

Complicating the picture further is the narrowing gap between U.S. and Japanese 10-year yields.

As this spread compresses:

The incentive to maintain yen-funded carry trades diminishes.

Capital can repatriate toward Japan.

U.S. asset markets face potential selling pressure.

This creates a structural constraint.

If U.S. Treasury yields fall aggressively, the carry unwind can accelerate. If yields remain elevated, domestic financial conditions stay restrictive.

In other words:

Policy choices are not made in isolation. Global capital flows limit how smoothly rates can adjust.

In Other Words:

Policy choices are not made in isolation. Global capital flows limit how smoothly rates can adjust.

Bottom Line

The narrowing US–Japan yield spread creates a structural constraint on how far U.S. rates can fall.

Gold: The Clearest Scorecard

Amid these mixed signals, gold has continued to attract institutional attention, with major banks, Citi Bank and UBS, raising price forecasts.

Gold does not respond to rhetoric alone. It responds to:

Real rates

Currency credibility

Policy uncertainty

Structural leverage

Its resilience suggests that markets are assigning incremental risk to fiat stability — not panic, but gradual repricing.

When gold strengthens alongside conservative central bank messaging and soft labor data, it implies that markets are hedging against policy constraints rather than celebrating policy clarity.

Gold is functioning as a neutral scoreboard.

Bottom Line

Gold is acting as the clearest scoreboard of rising fiat risk and policy uncertainty.

Closing Thoughts:

This week’s edition does not present a clean directional story.

It presents a constrained one.

The economy shows signs of strain.

The incoming Fed Chairman signals caution and discipline.

Global funding dynamics limit the ease with which yields can fall.

Gold continues to firm as a quiet hedge against fiat risk.

In such an environment, smooth adjustments become more difficult.

When policy flexibility narrows and external constraints tighten, markets tend to absorb the pressure through higher volatility rather than through orderly repricing alone.

The system is constrained — and in constrained systems, volatility risk tends to rise.

Look out for next week’s newsletter for further insight into the forces shaping today’s markets.