Newsletter Archive

Recent macro monday newsletter editions, organized by date.

Reviewing Bitcoin's Popular Stock-to-Flow Model

We set out to answer a simple question: does stock-to-flow tell us something real about Bitcoin, or does it only look powerful because it wraps a good story in precise numbers? What we found is that the scarcity story is compelling and may capture a real long-run relationship, but the model's famous price targets broke down once they met the real market. The practical takeaway is narrow but useful: give stock-to-flow modest weight as a way to think about shrinking new supply, and zero weight as a price target or a reason to size a position.

June 1st, 2026

Bottom Line

We set out to answer a simple question: does stock-to-flow tell us something real about Bitcoin, or does it only look powerful because it wraps a good story in precise numbers? What we found is that the scarcity story is compelling and may capture a real long-run relationship, but the model's famous price targets broke down once they met the real market. The practical takeaway is narrow but useful: give stock-to-flow modest weight as a way to think about shrinking new supply, and zero weight as a price target or a reason to size a position.

Thesis

The question behind this edition is not whether Bitcoin is scarce. It is. The question is whether that scarcity can be turned into a reliable price model. Plan B's stock-to-flow work became famous because it did two things at once: it translated the loose idea of "digital gold" into one simple number, and it attached that number to forecasts that looked unusually scientific, with headline fit statistics of 95% and 99.7%. We wanted to separate those two claims. What our research kept pointing back to is a balanced conclusion: stock-to-flow is a strong explanatory story about Bitcoin's hardness, but a weak tool for predicting where price will go on any useful timetable.

Evidence

What is scarcity here, and why did the idea spread so fast?

We should start with the basic concept, because the model's appeal begins there. Stock-to-flow measures hardness: the size of the existing pile divided by the amount of new supply created each year. In plain English, a high ratio means the pile is already so large, and the annual trickle of new supply so small, that producers cannot suddenly flood the market and dilute the asset. That is the intuition behind gold's long monetary history, and it is the same intuition Plan B applied to Bitcoin.

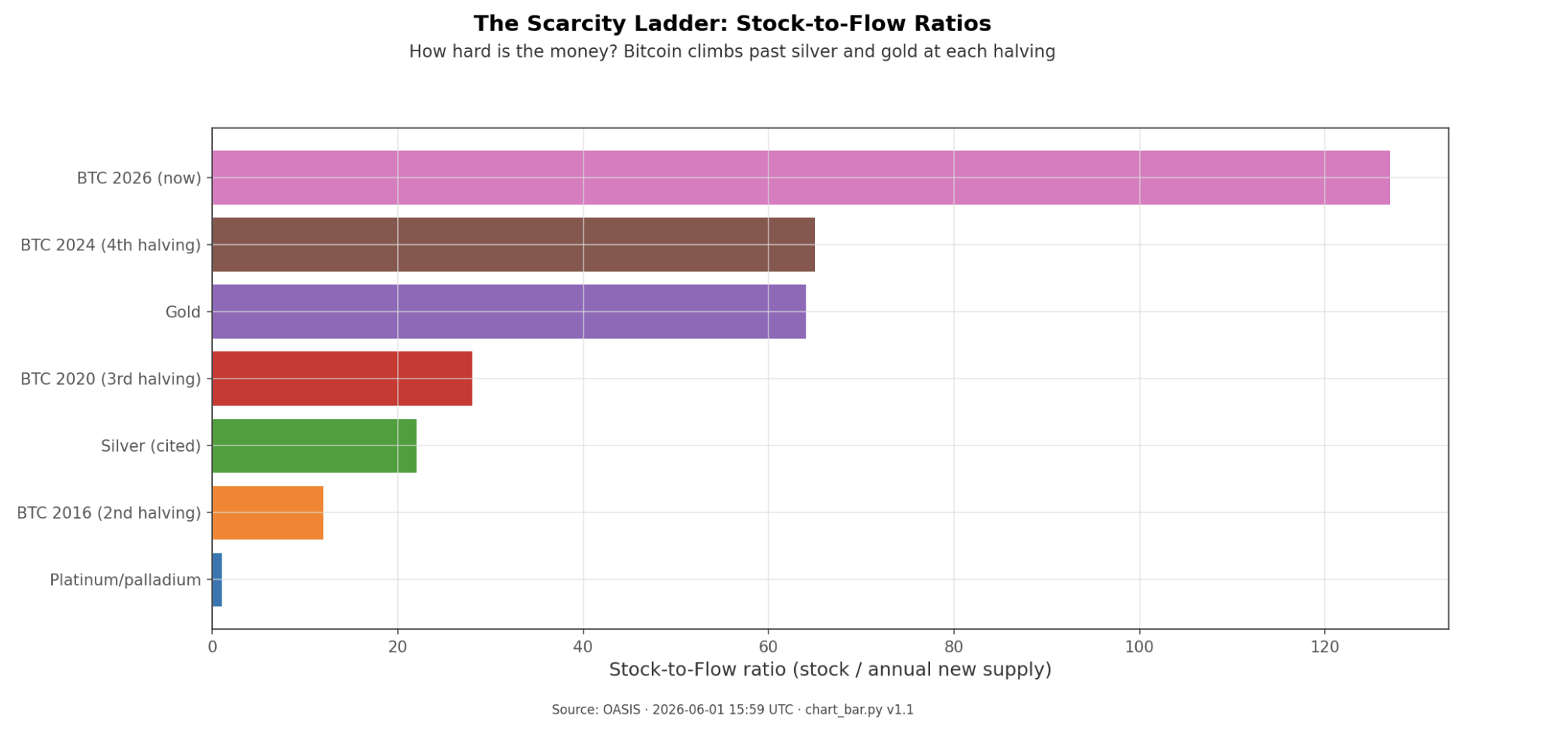

That framing matters because it gives Bitcoin's scarcity a concrete shape. Gold has traditionally been the benchmark hard money because its stock-to-flow sits around the low-to-mid 60s, meaning annual mine supply is tiny relative to the existing hoard. Bitcoin's issuance schedule is fixed in code, and every four years the halving cuts new issuance in half. That means Bitcoin's stock-to-flow roughly doubles each cycle: about 12 after the 2016 halving, about 28 in 2020, about 65 after the 2024 halving, and roughly 127 by May 2026. By this one measure, Bitcoin now screens as about twice as scarce as gold.

This is why the story traveled so far. It took a fuzzy slogan, "Bitcoin is digital gold," and turned it into a single number that could be ranked beside gold and silver. It was easy to explain, easy to share, and easy to remember: limited supply plus falling new issuance should mean a higher value over time. Our reading of the sources suggests that simplicity mattered as much as the math. A reader did not need a finance background to understand the claim.

The timing helped too. The model arrived just before the 2020-21 institutional wave, when large investors were already looking for a cleaner way to talk about Bitcoin as a hard asset rather than a speculative toy. The pseudonymous quant persona behind Plan B, plus the now-iconic rainbow-colored chart, gave the idea a strong social wrapper. And the statistics gave it authority. A model showing a 95% fit in the original version and 99.7% in the later cross-asset version does not just sound interesting; it sounds settled.

The model's claim was bigger than the story

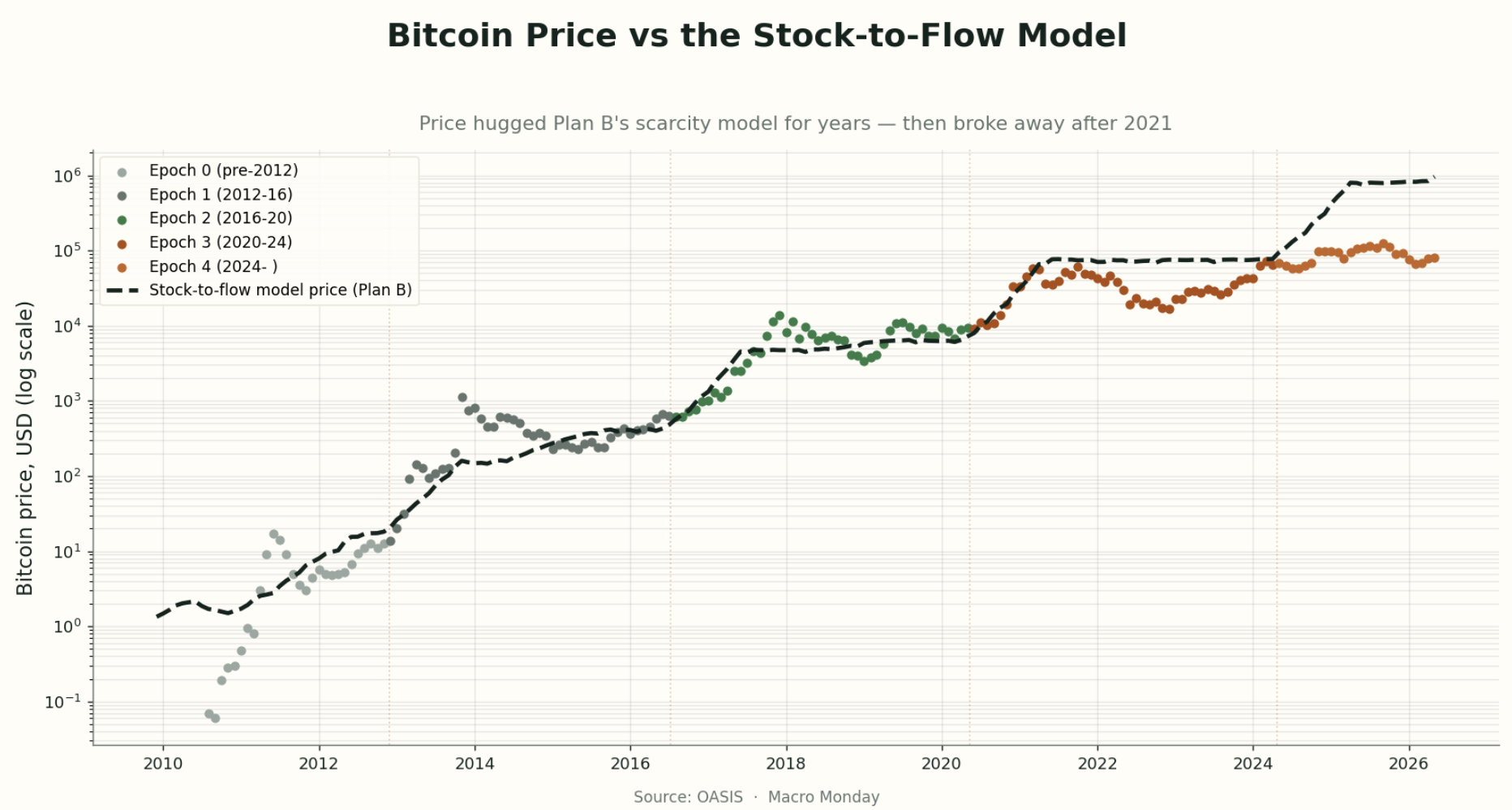

The next question we asked was what the models actually claimed, in plain terms. The original stock-to-flow model, published in March 2019, did not just say that scarcity matters. It said Bitcoin's market value could be explained by scarcity alone. Formally, it fit a regression of log market value on log stock-to-flow with an R-squared of 95%, and it projected that after the 2020 halving Bitcoin would be worth about $1 trillion in market value, or roughly $55,000 per coin.

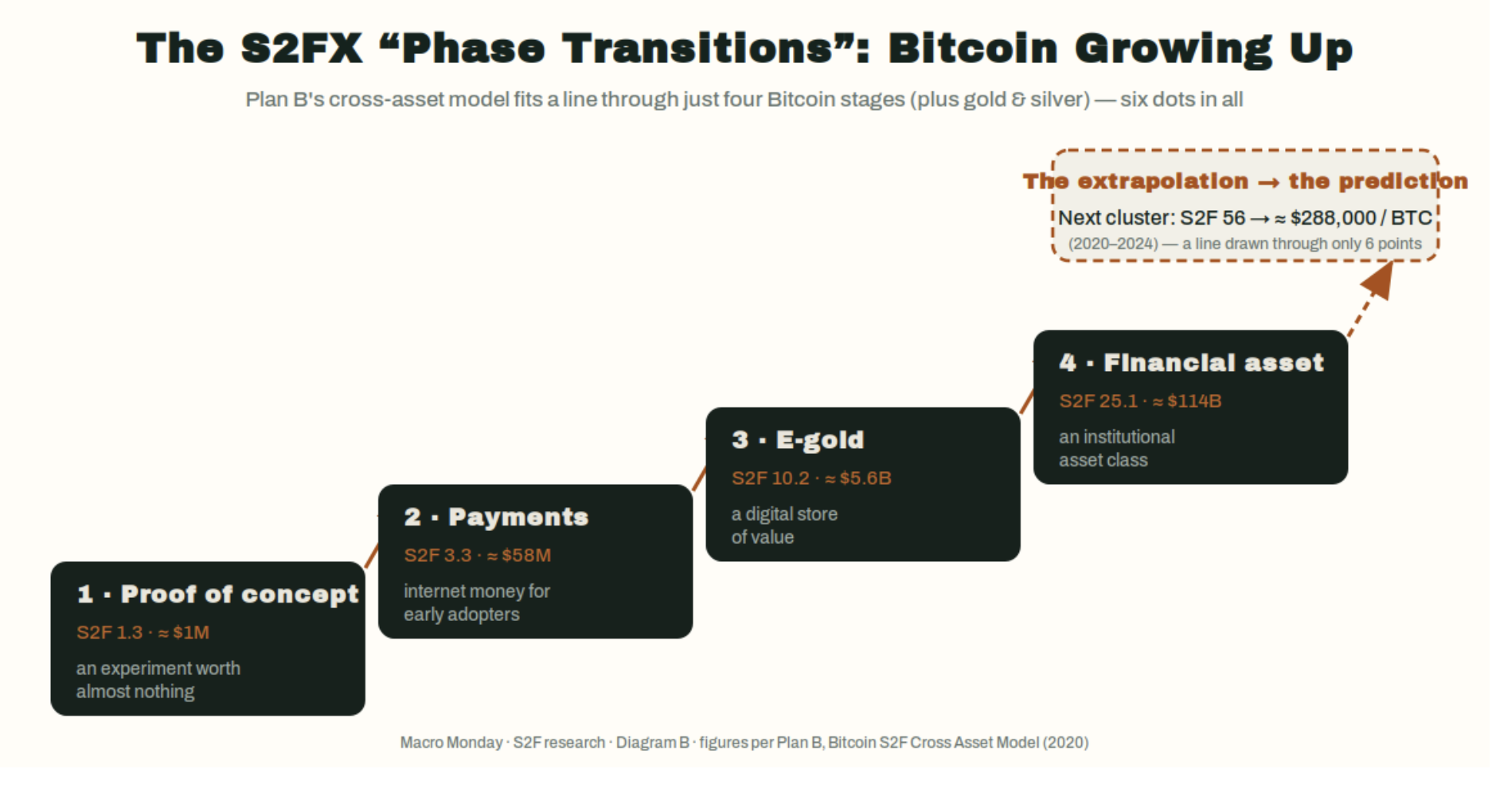

That was already a bold claim. It implied that one supply-side variable could explain most of Bitcoin's value. But the later cross-asset version, S2FX, made an even bigger leap. Instead of keeping Bitcoin on its own timeline, it lined up four Bitcoin phase clusters next to gold and silver as if they were points on one common ladder. In that version, Bitcoin moved from proof-of-concept to payments to e-gold to financial asset. The regression's reported fit rose to 99.7%, and the model's next target jumped to about $5.5 trillion in market value, or roughly $288,000 per Bitcoin during the 2020-24 cycle.

We can see why readers found this persuasive. The progression has a strong narrative rhythm. Bitcoin does not just get scarcer; it "grows up" into a new monetary role each cycle. The famous chart gave that thesis a single visual center: a line running through Bitcoin's history that made past rallies look like confirmations rather than surprises.

Plan B's response to the obvious market-efficiency objection also deserves fair treatment. Critics argued that if Bitcoin's supply path is public and fixed, the market should already price it in. His answer was not irrational. He argued that the market may systematically overestimate Bitcoin-specific risks, such as miner stress after halvings or broader failure scenarios, so as those feared outcomes fail to appear, the risk premium fades and price rises toward the model. We do not need to accept that as proven to see that it is at least a coherent defense.

That is an important distinction for this piece. The steelman is not "the model hit every number." It did not. The steelman is that the model points to a real supply mechanism, then adds a plausible behavioral explanation for why a public schedule might still matter in price.

Why the near-perfect fit should make readers more careful, not less

The problem is that a compelling mechanism is not the same thing as a reliable model. When we moved from the story to the model construction, the weaknesses became hard to ignore.

The first weakness is statistical. Both Bitcoin's price and Bitcoin's stock-to-flow rise over time. When two series trend upward together for long enough, a simple regression can produce a very high fit even if the underlying connection is weak or meaningless. That is the core spurious-regression critique. In one sharp summary from the critique literature, the regression may be doing little more than estimating Bitcoin's historical growth trend.

The second weakness is that when researchers try to strip out that shared time trend, the magic largely disappears. In the critique cited in our research, the stock-to-flow coefficient is no longer statistically significant once time fixed effects are included, with a reported p-value around 0.39. A separate critique found that plain circulating supply tracks market capitalization about as well as stock-to-flow does, and that after correcting for autocorrelated residuals, the stock-to-flow term is effectively zero. In plain language: once the time trend is handled more carefully, the model stops looking uniquely informative.

The third weakness is conceptual rather than statistical. The model looks only at supply. Price does not. Price is always the meeting point of supply and demand. A pure scarcity metric can tell us that new supply is shrinking, but it cannot tell us whether demand will surge, stall, or collapse. That omission matters because the largest real price moves are often demand-driven.

The fourth weakness is the gold comparison itself. Gold is the benchmark hard asset precisely because its stock-to-flow has been stable and high for a very long time. Yet gold's market value did not stay remotely stable alongside that ratio. Over roughly the past century, its stock-to-flow sat near 60 while its value ranged from about $60 billion to about $9 trillion, roughly a 150-fold swing. That does not mean scarcity is irrelevant. It means scarcity alone is not a law of value.

The fifth weakness sits inside the cross-asset model. Its famous 99.7% fit came from six points: four hand-grouped Bitcoin clusters plus gold and silver. That is too small and too curated a sample to carry the weight many readers put on it. The result may be interesting as a framing device, but it does not amount to proof.

The cross-asset visual helps explain both the attraction and the problem. It is elegant. It is memorable. But it also asks the reader to accept that these selected clusters and metals belong on one regression line, which is a much larger assumption than the chart's neatness suggests.

This is where the balanced reading becomes important. We should not confuse "there is a plausible supply mechanism" with "the model's coefficients and targets are trustworthy." The first claim may survive. The second is much harder to defend.

The real track record was strong until it wasn't

The hardest test for any model is not whether it tells a compelling story, but whether its forecasts hold up after readers start relying on them. Here the picture changes meaningfully.

For a while, stock-to-flow genuinely looked vindicated. From roughly 2015 through late 2021, Bitcoin's price tracked the model line closely enough that each rally looked like fresh proof. The 2020 halving was followed by a run to Bitcoin's roughly $69,000 peak in November 2021, which seemed close enough to the original post-halving ~$55,000 call to reinforce confidence rather than weaken it.

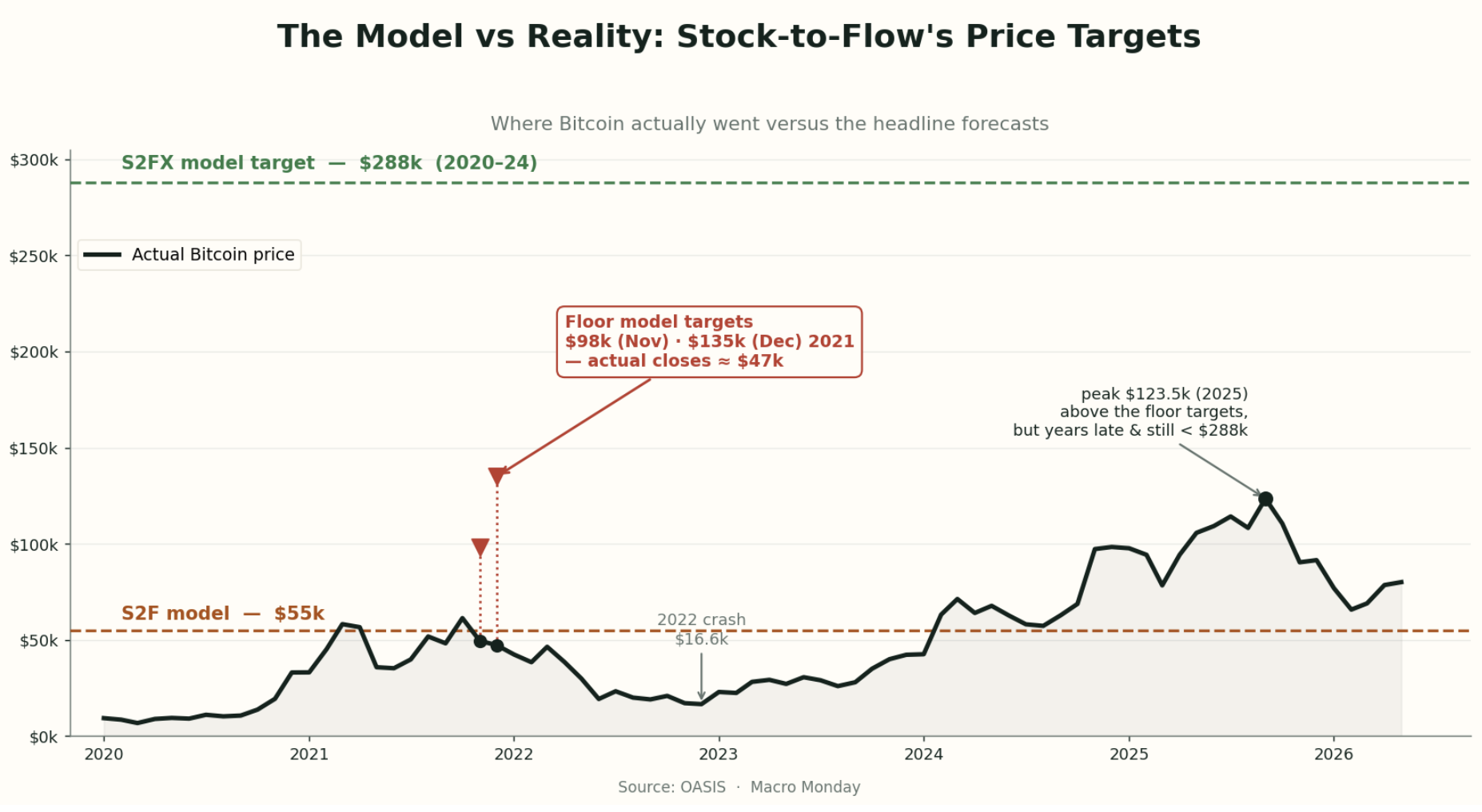

The trouble came when the targets got more explicit. Plan B's separate short-term floor model called for $98,000 by November 2021 and $135,000 by December 2021. Bitcoin instead closed those months near $49,484 and $47,299. Those are not narrow misses. They are misses by about half.

That miss mattered for two reasons. First, it broke the aura of precision. Second, it forced a distinction between the failed floor model and the supposedly still-intact long-term stock-to-flow model. Plan B explicitly conceded "Nov98K & Dec135K miss = FLOOR MODEL FAIL ... S2F MODEL INTACT." Critics reasonably read that as moving the goalposts, especially because earlier messaging had implied that a sub-$100,000 December 2021 price would invalidate the stock-to-flow thesis.

Then came the 2022 collapse. Bitcoin fell to about $16,612 in December 2022, a drawdown that is much easier to explain through demand destruction than through a supply schedule that had not changed. This is exactly the scenario the critics had in mind. A model that only tracks shrinking issuance has no way to see a demand-driven bear market coming.

The later outcome did not repair the forecast record. Bitcoin did eventually trade above $98,000, but not until 2025, years late, and it never reached the cross-asset model's $288,000 target for the 2020-24 cycle. The eventual peak cited in our research was about $123,521 in September 2025. That is materially above the floor targets, but still far short of the cross-asset projection and too late to count as a clean success.

This is the paragraph where the tension has to be named plainly. On one side, the early fit and post-halving rally gave stock-to-flow a real appearance of confirmation. On the other, the dated targets failed, the 2022 collapse exposed the missing demand side, and the cross-asset target never arrived. Those signals do not share a clean "the model works" story. If we have to lean one way, our research leans toward the track record being too weak to justify treating stock-to-flow as a forecasting tool.

The steelman is real, but it leads to humility, not vindication

Still, the case against stock-to-flow is not complete without the strongest defense. Our research found one argument critics cannot dismiss lightly: cointegration.

In simple terms, cointegration asks whether two series that wander over time still maintain a stable long-run relationship. That is different from saying they merely trend up together. The steelman is that Bitcoin market value and stock-to-flow may be genuinely linked in this long-run sense. Nick from BTConometrics argued that the relationship appears cointegrated and could not be falsified. More strikingly, Marcel Burger, who initially criticized stock-to-flow as spurious, later ran three cointegration tests expecting to reject the link and could not. He publicly apologized for dismissing it too quickly.

That matters. An adversarial replication failing to debunk the relationship is not nothing. It raises the possibility that there is a real long-run association here, not just a visual coincidence on a chart.

The mechanism also remains believable. Halvings are real. They mechanically cut new issuance in half. Holding demand constant, that is a genuine supply shock. And Plan B's efficient-market rebuttal remains logically coherent: a public model can still appear to "work" if the market persistently overprices Bitcoin's risks and gradually unwinds that premium as feared breakdowns fail to occur.

But this is where the piece has to stop short of over-correcting. Cointegration is not proof of causation. The data history is still short, on the order of a decade or a bit more, with only a few halvings to learn from. And even if the long-run relationship is real, it says little about short-term price and did nothing to save the failed floor model. So the strongest defense of stock-to-flow still ends in humility. It may point to a real long-horizon scarcity link, but it does not rescue the model as a timing or target-setting tool.

That is the balanced answer the owner asked for. Readers should give equal weight to two truths at once. The scarcity mechanism is not nonsense, and the long-run relationship may be more than a mirage. At the same time, the model's precision is overstated, its construction has real weaknesses, and its public targets have already failed in ways that matter.

Implications

What the findings suggest is a cleaner way to use stock-to-flow. Use it as a language tool, not as a valuation tool. It helps explain one true thing about Bitcoin: new supply keeps shrinking on a known schedule, and that is part of why Bitcoin can plausibly carry a hard-money premium. But that is a very different claim from saying the next halving points to a specific price. For readers, the practical line is straightforward: stock-to-flow can help separate a scarcity narrative from a price forecast. Give it modest weight when thinking about Bitcoin's monetary character, and no weight when deciding on targets, timing, or position size.

What to Watch

Whether future stock-to-flow commentary stays in the narrow lane of scarcity and market structure, or starts turning back into dated six-figure target claims.

Whether the next cycle produces evidence of a stable long-run link again, while remembering that even a long-run link would still not validate short-term price forecasts.

Whether demand-side shocks, such as another sharp risk-off phase, once again dominate the price path despite Bitcoin's mechanically shrinking new supply.

Whether readers and analysts keep the key distinction clear: scarcity may help explain why Bitcoin can carry a premium, but scarcity alone has not proved able to forecast where that premium will trade.

Look out for next week’s newsletter for further insight into the forces shaping today’s markets.

A Framework for Understanding the Oil Market

We set out to build a practical framework for reading oil, and the research kept pointing back to a simple structure: a US-led supply base, an Asia-led demand base, four distinct regional markets, and a small set of price levers led by OPEC spare capacity, inventories, the dollar, and the crude-to-products margin channel. The strongest evidence is that supply has re-centred from OPEC to the United States, with OPEC's share of world production falling from 35.2% in 2000 to 27.5% in 2024 while US total liquids output more than doubled from 9.1 to 22.8 mb/d, even as demand has re-centred toward China and India. For readers, the point is that oil is easiest to misread when we start with the headline scare; the more reliable sequence is to start with the market's structure and levers, then ask whether a geopolitical event is actually converting into a measurable supply shock.

Bottom Line

We set out to build a practical framework for reading oil, and the research kept pointing back to a simple structure: a US-led supply base, an Asia-led demand base, four distinct regional markets, and a small set of price levers led by OPEC spare capacity, inventories, the dollar, and the crude-to-products margin channel. The strongest evidence is that supply has re-centred from OPEC to the United States, with OPEC's share of world production falling from 35.2% in 2000 to 27.5% in 2024 while US total liquids output more than doubled from 9.1 to 22.8 mb/d, even as demand has re-centred toward China and India. For readers, the point is that oil is easiest to misread when we start with the headline scare; the more reliable sequence is to start with the market's structure and levers, then ask whether a geopolitical event is actually converting into a measurable supply shock.

Thesis

We began with a broad question: what is the cleanest way to understand the oil market without collapsing into daily noise or one-cause stories? What we found is a framework that is simpler than the flow of headlines but more demanding than the usual narrative. The market is anchored by a few supply centers, a few demand centers, three pricing benchmarks, and two chokepoints, but price does not respond to all of them equally. Our work kept pointing back to buffer variables and transmission channels: OPEC spare capacity as the main volatility gate, US shale as the slow-response cap on sustained spikes, inventories as a deviation-from-normal signal, the US dollar as a macro overlay, and the crack spread as the path from crude into retail fuel. We then used that framework to stress-test oil history and, only at the end, to evaluate Iran and the Strait of Hormuz as a case study in when a familiar market narrative is wrong and when it becomes literally true.

Evidence

The map is smaller than it looks

The first question we were trying to answer was basic: what, concretely, is the global oil market? The structural map is compact. On the supply side, the three anchor producers are the United States, Saudi Arabia, and Russia. In 2024, US total liquids output reached 22.84 mb/d, with 13.23 mb/d of crude, versus roughly 9.9 mb/d for Russia and 9.2 mb/d for Saudi Arabia. On the demand side, the three anchor consumers are the United States at about 20.4 mb/d, China at 16.2, and India at 5.4.

The pricing side is similarly concentrated. WTI remains the North American benchmark, Brent the main seaborne global benchmark, and Dubai/Oman the benchmark for crude sold into Asia. The physical plumbing is narrow enough that two chokepoints dominate transmission risk: the Strait of Malacca at 23.7 mb/d in 2023 and the Strait of Hormuz at 20.9 mb/d, or about one-fifth of world oil use. That matters because any supply disruption or geopolitical stress has to show up somewhere, and these nodes are where the market registers it.

This is the first discipline of the framework. Oil may look like one global tape, but the useful starting point is not "price went up, why?" It is "which node moved?" The answer usually sits with a benchmark, a supply anchor, or a chokepoint rather than with the headline itself.

The center of gravity moved: supply to the US, demand to Asia

The next question was what changed in the market's center of gravity. On supply, the answer is the US. OPEC's share of world production fell from 35.2% in 2000 to 32.9% in 2010 and 27.5% in 2024, even though OPEC broadly held output flat. What changed was non-OPEC growth, and especially US growth. US total liquids output rose from 9.06 mb/d to 22.84 mb/d over that same span, making the US the world's largest producer by 2024 and the largest crude producer at 13.23 mb/d, ahead of Russia at 9.89 and Saudi Arabia at 9.23.

On demand, the answer is Asia. China's oil consumption rose from 2.33 mb/d in 1990 to 16.37 in 2024, about a seven-fold increase. India's rose from 1.17 to 5.60 mb/d, about a five-fold increase. OECD Europe, by contrast, stayed roughly flat, moving from 13.78 to 13.47 mb/d over the same period. The United States remains the single largest consumer at about 20.4 mb/d, but China has closed the gap materially, moving from well under half the US level in 2010 to roughly four-fifths by 2024.

OPEC's output (blue) stayed roughly flat while non-OPEC supply (orange) — led by US shale — drove nearly all the growth in world production; OPEC's share of the total fell from about 35% in 2000 to 27.5% in 2024. The shift of demand toward Asia is the second half of the same re-centring.

That double re-centring matters because it changes how to read risk. The market is no longer dominated by an OPEC-only supply story or a West-only demand story. It is better understood as a US-led supply expansion meeting Asia-led demand growth. That is also why chokepoints matter so much: the biggest structural dependency in the system is not US consumption, but Asia's need to import large volumes of crude through narrow sea lanes.

One headline price, four different regional machines

We then asked what sits underneath the single headline oil price. The answer is four regional markets that are linked, but not interchangeable.

The Americas are the self-sufficient machine. They are anchored by US production and price off WTI, which trades at a discount to Brent. The spread has averaged about -$5.85 to Brent, which is the market's way of pricing a region that broadly covers its own crude needs but still faces transport and export constraints. Put simply, WTI tends to be cheaper because US barrels are abundant and have to be moved out to the world market. This region is comparatively insulated on physical supply.

Europe is the mature import-dependent machine. It prices off Brent and pays the seaborne benchmark because it is structurally short crude. Its demand profile is mature rather than fast-growing, and after 2022 it became more dependent on replacement seaborne flows after losing much of its prior Russian supply path.

Asia-Pacific is the demand-and-refining engine. It prices off Dubai, carries about 35% of global refining capacity, and imports heavily because its demand far exceeds its production base. China alone nets roughly 11 mb/d of crude imports. This region is where the physical consequences of a Gulf disruption matter most.

The Middle East is the export-hub and balancing machine. The Gulf producers collectively pump about 24 mb/d and, crucially, hold much of the world's spare supply. Their oil is sold into other regions, especially Asia, and much of that flow runs through Hormuz. That is why the most consequential linkage in the whole map is the Middle East-to-Asia axis: the world's largest holder of spare capacity selling to the largest and fastest-growing import market through the least easily bypassed route.

This framing helps when we get to Hormuz. If Asia is the import engine and the Gulf is the export valve, then a Hormuz event is not first a generic fear story. It is first a regional flow story that may or may not widen into a global price shock.

What really moves oil prices

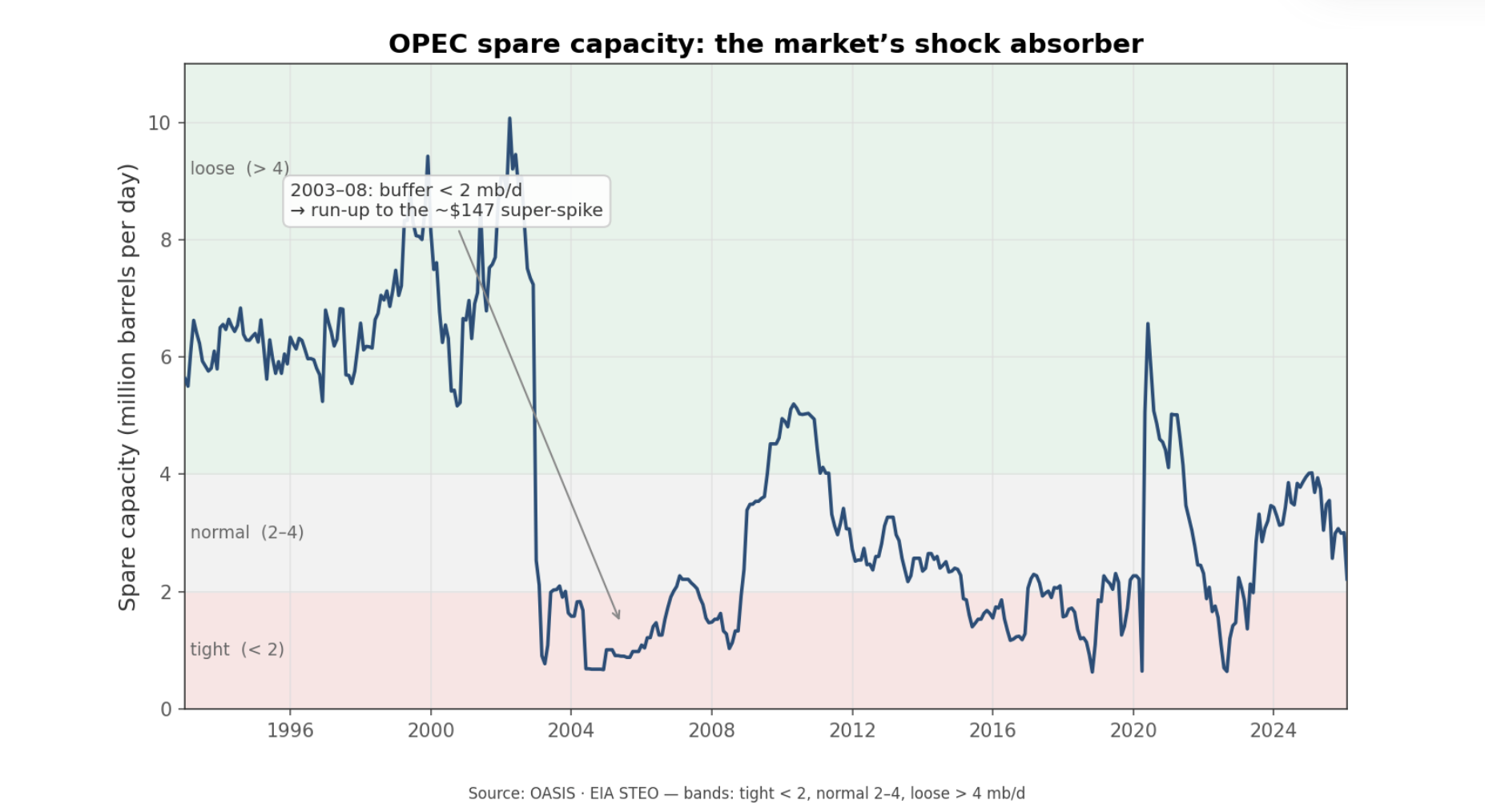

Once the regional structure was clear, we turned to the levers that actually move price. The strongest one in the framework is OPEC+ spare capacity. What we found is that it matters most as a volatility gate rather than a simple level setter. The only sustained period it fell below the 2 mb/d tight threshold was 2003-08, when it averaged 1.45 mb/d and the market ran into the super-spike toward roughly $147. The two loose-buffer regimes, the late 1990s and 2020, line up with the two major price routs. Over 1993-2026 the long-run mean is about 3.73 mb/d. The relationship to price is negative, meaning tighter spare capacity usually goes with higher oil prices, but the bigger practical point is simpler: when the cushion is thin, the market has less room to absorb a shock; when the cushion is large, shocks are easier to contain.

Spare capacity is the market's shock absorber. The most violent oil moves tend to happen when that buffer is already thin — the only sustained stretch below 2 mb/d, in 2003–08, ran straight into the ~$147 super-spike.

The next lever is US shale. The work here asked whether shale changed oil from a fixed supply market into a more elastic one. The evidence says yes. Rig-count changes lead production with a statistically meaningful relationship, and output per active rig nearly tripled from about 9,600 to 25,800 bbl/d between 2010 and 2024. In plain language, shale made US supply more responsive. A price shock no longer has to stay in place for years to invite new production; it can draw a domestic response within a few quarters.

Russia under sanctions was the third upstream test. Here the findings were more cautionary than dramatic. Russian output fell only modestly, from around 10.4 to 10.0 mb/d between 2021 and 2026, while the barrels Europe stopped buying were absorbed by Asia. We should read that as a flow-map story more than a supply-destruction story. It is a useful warning because the market often confuses route disruption with production loss. Sometimes they overlap, but not always.

Inventories and the dollar add the macro layer. The OECD-wide commercial stock signal matters more than the weekly US print. In a monthly decomposition of WTI returns, OECD stock changes carry a clear negative relationship with price, while US weekly stocks are only marginally useful on their own. The dollar is the strongest single measured driver in that model: when the dollar strengthens, oil usually becomes more expensive in local-currency terms for the rest of the world, which tends to weigh on demand and price. Even then, about 90% of the variance remains unexplained. That is a standing warning built into the framework: even a serious model leaves most month-to-month oil movement unexplained.

Finally, we wanted one downstream channel that links crude to the end user. The 3-2-1 crack spread does that. It measures the gross margin from turning three barrels of crude into two of gasoline and one of diesel. It averages about $10.6/bbl over 1986-2026, with a typical range of roughly $2-24, and moves cyclically with product tightness and refinery utilization. In simpler terms, it is the margin bridge between crude and the fuels households and businesses actually buy. That makes it the key translation layer from crude-market stress into pump-price pressure.

Taken together, these levers answer a question readers often ask implicitly: what should we weight heavily, and what should we discount? The framework's answer is spare capacity first, then the shale response function, then broad inventory deviations and the dollar, with the crack spread as the channel into products. The weekly US stock print matters much less than its visibility suggests.

History gives two durable rules

With the structural map and levers in place, we wanted to know whether history actually respects the framework. Across six episodes since the 1980s, two patterns dominated.

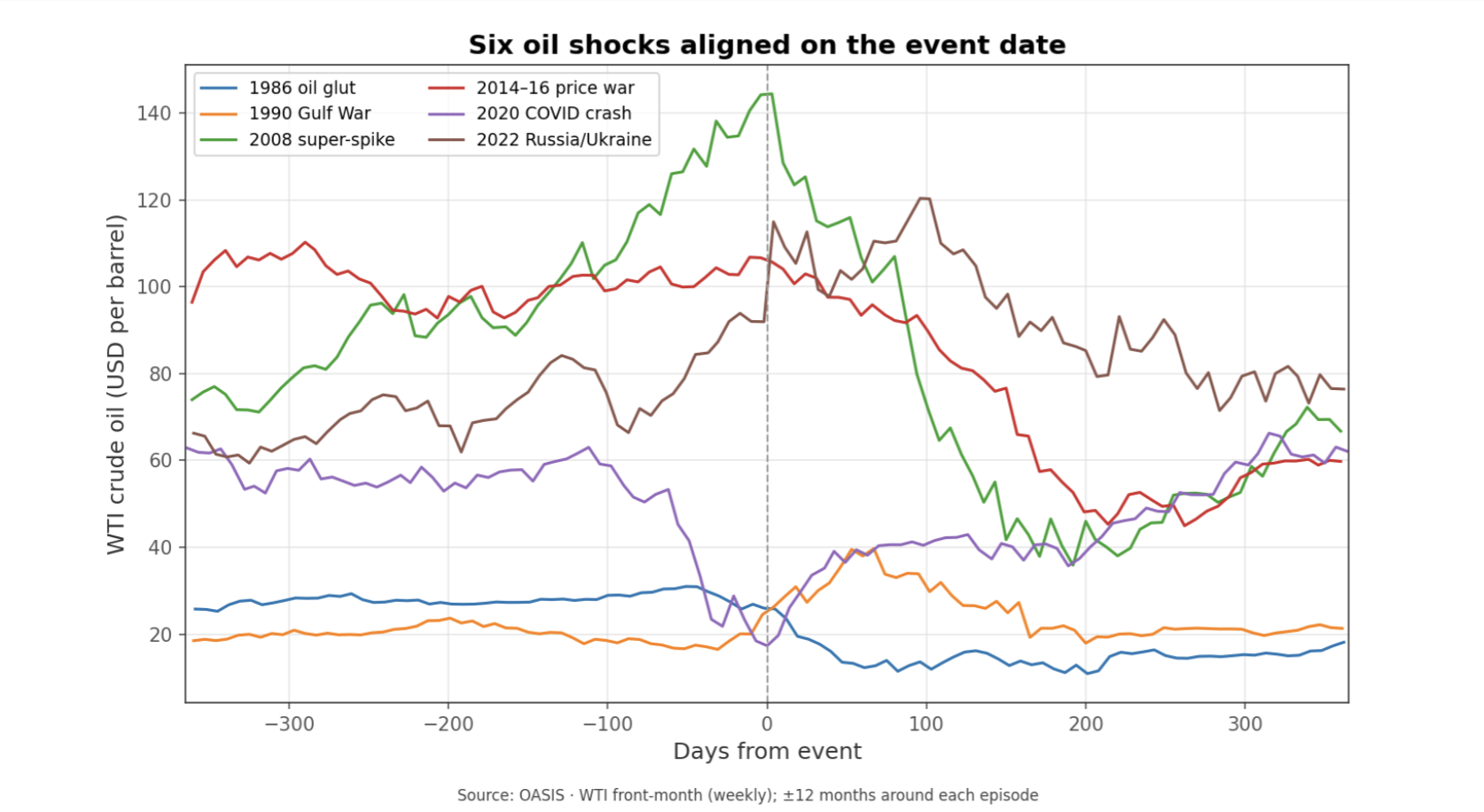

The first is that OPEC spare capacity governs amplitude. The most violent events formed on thin buffers. In 2008, WTI peaked at $144.41 and then collapsed to $35.88 by early 2009. In 2022, WTI rose to a $120.34 peak. In both cases the market was running on roughly 1-2 mb/d of spare capacity. In 2020, by contrast, the crash drove the buffer loose to around 4.2 mb/d.

The second pattern is that geopolitical spikes reverse unless barrels actually disappear. The 1990 Gulf War is the cleanest example. Iraqi and Kuwaiti output fell by about 4 mb/d combined, WTI jumped from roughly $16 to $40 in three months, and Saudi Arabia ramped from 6.4 to 8.1 mb/d to backfill the loss. Six months later WTI was 10.5% below its invasion-week level. The 2022 Russia/Ukraine shock showed a similar round trip. WTI rose 25% the week after the invasion and peaked near $120, but six months later it was only 1.1% above its invasion-week level because Russian barrels were rerouted rather than removed. Most tellingly, a model that included a broad geopolitical-risk index attributed just 0.4% of WTI's movement to it in that episode. In plain language, the war mattered, but geopolitical fear on its own explained almost none of the price move once the actual supply path was accounted for.

History leaves two working rules: thin spare capacity makes moves more violent, and geopolitical spikes tend to fade unless barrels are truly removed from the market.

That leaves us with a strong prior before we even turn to Hormuz. If the market is reacting to a geopolitical scare but barrels still flow, the move should tend to round-trip within months. If a violent move persists, the reason is usually not the headline in isolation but the physical supply channel the event touched. And across these episodes the unexplained share stays large — 89–98% of the weekly moves in the major post-2008 shocks — which should keep us modest about any tidy narrative.

Hormuz is the right final test

Only after building the framework did we turn to Iran and the Strait of Hormuz as the closing case study. The first point is structural importance, and on that the data are straightforward. About 20.9 mb/d moved through Hormuz in 2023, around 20.4% of global liquids output, making it the second-busiest chokepoint by raw volume and the one with the fewest practical alternatives. On importance, the narrative is right.

The second point is how the 2026 disruption is best measured. Official transit-volume series are published with a long lag, so the scale of the throughput collapse is read more reliably from price and shipping signals than from headline flow counts — and on those signals the disruption is unmistakable, with tanker traffic through the strait reported down more than 80% at the peak.

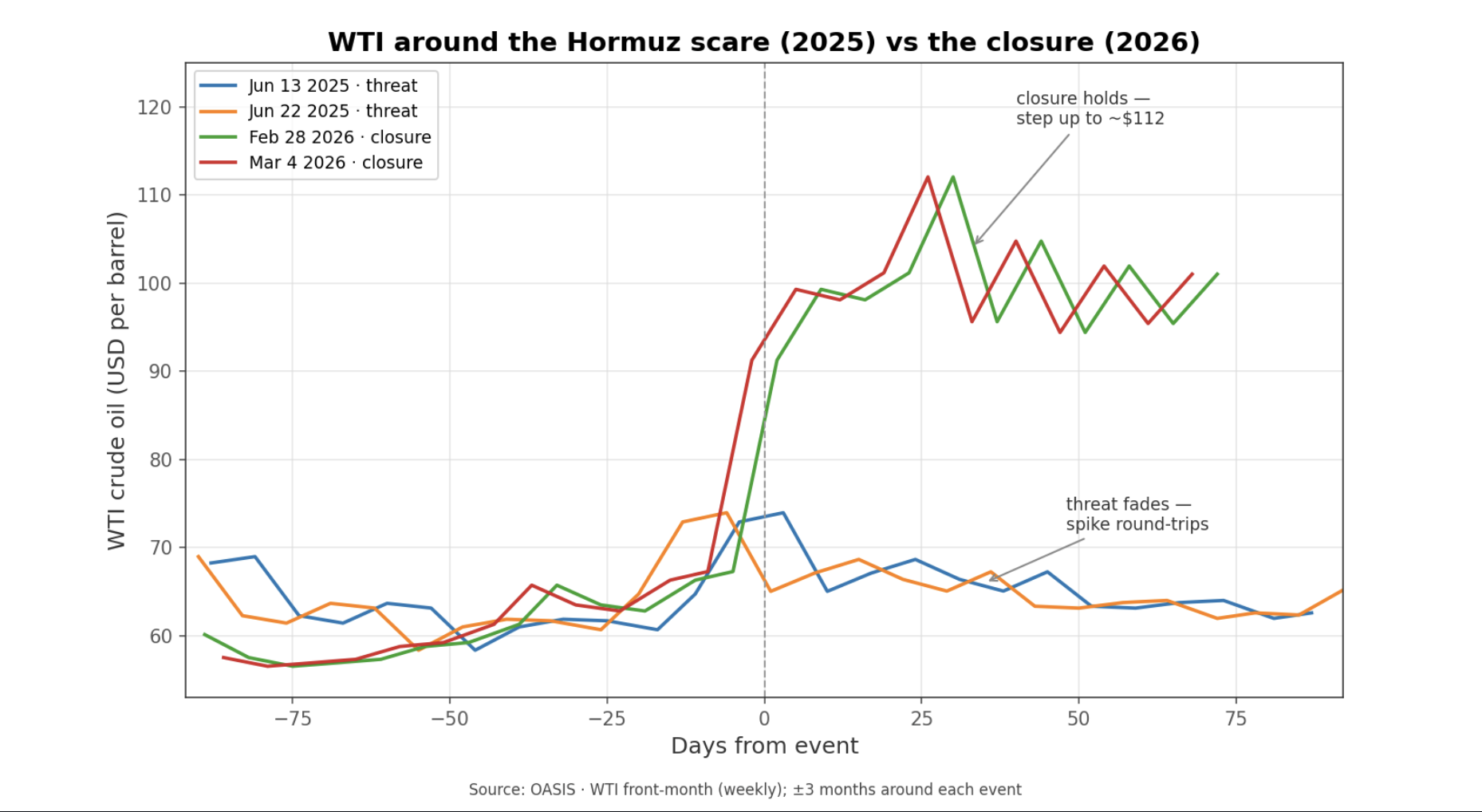

The third point is the distinction between a threatened closure and a realized one. In June 2025, the common narrative was that Iran and Hormuz were driving oil higher. WTI spiked about 23% and then round-tripped within two weeks. Brent-WTI narrowed to about +$2.46, below its +$5.19 24-month average, and Dubai showed no Asian premium. That is what a fear spike looks like when the physical system does not break.

The 2026 closure looked different. Brent-WTI widened sharply, peaking near +$18 in April and averaging roughly +$11 over the disruption window. Dubai, however, did not gain an Asian premium. Its discount to Brent blew out to -$13.7 in March and -$24.4 in April. That is a crucial finding because it inverts the naive script. The market response was not Asia bidding Gulf crude higher. It was Gulf crude being stranded behind the strait, depressing the Gulf marker relative to the globally deliverable Atlantic benchmark. In other words, the spread pattern confirms a real disruption, but by showing trapped supply rather than a classic scarcity premium in Dubai.

The two June 2025 scare dates (blue, orange) spike and round-trip within weeks; the two 2026 closure dates (green, red) step up to roughly $112 and hold. A threat that faded versus a closure that realized.

The supply data align with that reading. Over the recent 12 months, WTI's tightest relationships were with OPEC production at -0.95 and OPEC spare capacity at -0.94. OPEC output fell from 30.78 mb/d in February 2026 to 20.16 by May, and spare capacity collapsed from 3.01 to 0.03. The US dollar and US production explained essentially nothing over that window. Put simply, the oil market was moving with Gulf supply conditions, not with US supply or currency conditions. This is the key interpretive point: in 2026, we cannot cleanly pit "Hormuz" against "fundamentals," because the closure is itself the supply fundamental. The shock shows up as lost deliverable Gulf output and vanished usable spare capacity.

The fuller statistical picture reinforces the same lesson. In a decade-long monthly model (2015–2026), OPEC production accounts for 12.3% of WTI's movement, OECD inventories 3.7%, Russia 2.1%, and a direct "Hormuz event" term just 0.85% — with roughly 80% unexplained. That small event share should not be over-read: it swings from well under 1% to about 8% depending on how the model is built, because the Hormuz term is statistically entangled with the OPEC supply collapse the closure caused. The honest takeaway is the range, not any single figure — and the mechanism matters more than the percentage: the closure moved price through the supply channel, not as a standalone headline premium.

So the balanced answer is clear. When Hormuz is only threatened, the "Iran drives oil prices" story usually overstates the evidence. When Hormuz is actually closed, the story becomes correct, but correct as a physical Gulf-supply shock rather than as a pure geopolitical premium. And even there, we should remember that roughly 70-90% of month-to-month oil movement stays statistically unexplained. The framework helps us read the event better, but it does not turn oil into a one-variable market.

Implications

What the research suggests is a practical reading order for oil. Start with the structure: who produces, who consumes, which benchmark is moving, and whether the key regional spreads are confirming a real seaborne disruption. Then check the levers: spare capacity, broad inventory deviations, the dollar, and whether shale can respond over the next few quarters. Only after that should we decide whether a geopolitical narrative deserves to be treated as a genuine fundamental shock. For readers tracking macro transmission, the crack spread remains the useful bridge from crude to consumer prices, while the Hormuz case study leaves a clear operating rule: fade the familiar scare until spread and supply data confirm conversion, but once production and deliverability actually break, treat the move as a real supply event rather than a temporary headline premium.

What to Watch

Brent-WTI versus its roughly +$5 norm; sustained widening is the cleanest real-time sign that a Gulf or seaborne disruption is becoming global rather than staying local.

Dubai-Brent; a sharply deeper Dubai discount can signal stranded Gulf supply. It is a monthly gauge, so it confirms a shift more slowly than the daily Brent-WTI spread.

OPEC production and spare capacity together; if output falls and spare capacity compresses toward zero, the market is no longer pricing fear but an actual supply constraint.

OECD commercial stocks relative to normal, not just the weekly US crude print; the broad inventory deviation carries more signal than the headline Wednesday number.

Humility on any single-cause story; roughly 70-90% of oil's month-to-month move stays statistically unexplained, so treat any precise "X% was Hormuz" attribution with skepticism.

Look out for next week’s newsletter for further insight into the forces shaping today’s markets.

The Four Eras of Liquidity

This week we examined whether the four-era framework used to describe modern monetary history - the gold-standard period before 1971, the post-Nixon fiat era from 1971 to 2008, the post-financial-crisis QE era from 2008 to 2020, and the post-COVID era from 2020 to today - actually shows up in market data.

May 18th 2026

Bottom Line

The four-era framework does show up in market data, and the post-COVID era stands out as the most money-sensitive market period on record, with stocks now responding about three times more strongly to global money supply — the broad measure of money in the economy, including cash, bank deposits, and the credit banks create when they lend — than in earlier eras. Practically, that changes which liquidity measure matters most, which assets tend to move together, and how to read a record high like today's.

Thesis

We began with a basic question: is the four-era framework a real feature of markets, or just a tidy historical story? What we found is that the breaks are real enough to use, and each era carries a distinct pattern in how liquidity and assets interact. The headline finding is simple: markets have become more responsive to the global money supply over time, with the strongest link in era 4, the post-COVID period that began in March 2020. This week, we want to share that map at a high level because it helps explain the current regime.

What Changed

A couple of weeks ago we looked at the shape of the US economy through GDP. This week we shift from economic structure to monetary structure: not what the economy is made of, but the money-supply backdrop that increasingly shapes market behavior.

What changed is that the four-era framework now has direct research backing. We tested it across stocks, bonds, gold, Bitcoin, and home prices, and the relationships clearly changed across eras.

Evidence

The eras are real

We organize modern market history into four eras: pre-1971 when the dollar was still tied to gold, 1971-2008 after Nixon broke that link, 2008-2020 when QE became a defining policy tool, and 2020-present when the COVID response reset the liquidity regime.

We wanted to know whether the data could find those breaks on its own. It largely did. A statistical break-detection routine picked up the 2008 turn in G5 central-bank balance sheets at 2008-10-01 and the 2020 turn at 2020-04-01. Global money supply also identified the 2020 break within 2.6 months.

That tells us the framework is not just a neat narrative. The measurable series bend around the same turning points. Era 1 remains untestable directly because the liquidity data do not reach back far enough.

Money has mattered more in every new era

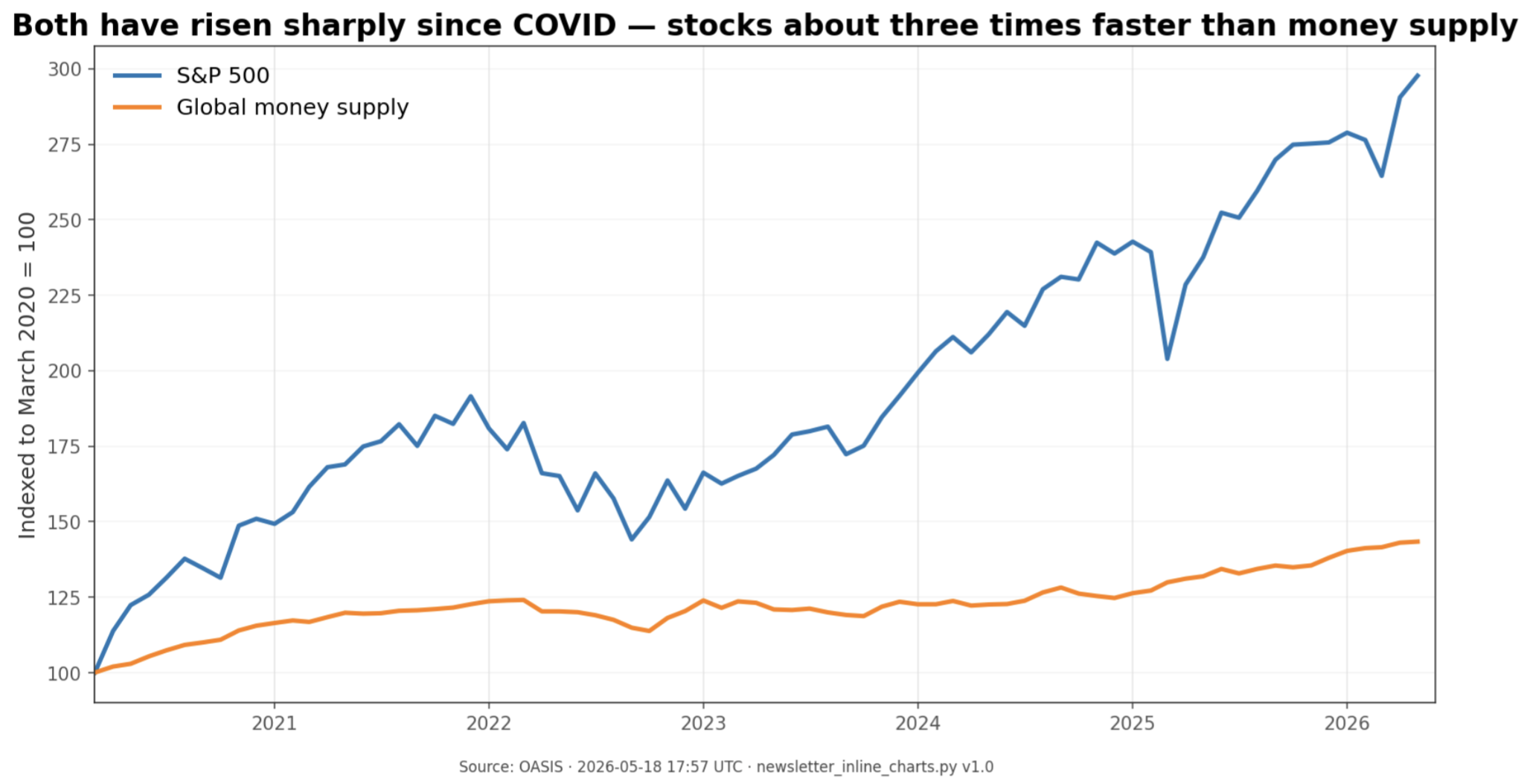

The clearest high-level finding is that each new monetary era made stocks more responsive to the global money supply. In era 2, a 10% rise in global money supply lined up with about an 11% rise in the S&P 500 on average. In era 3, that became about 21%. In era 4, it became about 30%. That is the progression from 1.09 to 2.12 to 3.05.

Put plainly, the money supply has gone from an important backdrop to a much stronger force inside the equity regime. The fit also stays unusually high across eras, explaining about 88% to 95% of long-run S&P 500 movement depending on the period. Gold and bonds follow the same direction too: their coupling with liquidity also strengthens from era 2 through era 4.

From era 2 to era 4, the S&P 500 became far more sensitive to global money supply growth. Think of it this way: a 10% rise in global money supply lined up with roughly 11% stock gains in the earlier measurable era, about 21% in the QE era, and about 30% in the post-COVID era.

In era 4, the kind of money matters

Consider an analogy: think of money as the water in a swimming pool, and asset prices as the boats floating on top. In era 4, the boats are still being lifted by rising water, but we have to be careful about which waterline we are measuring.

There are two useful layers. Central-bank balance sheets track the money central banks create directly. Broad money supply tracks that base plus deposits, credit creation, and near-cash moving through the wider system. In era 4, those two layers decoupled: central-bank balance sheets shrank under QT while money supply kept expanding.

That distinction helps explain the S&P 500's latest all-time high. On 2026-05-11, SPX reached 7,408. Through the money-supply lens, that high looks supported, with about 88% of the long-run fit explained and the index only slightly below trend. Through the central-bank-balance-sheet lens, the fit is weak and the market looks more stretched. The disagreement is the finding: in era 4, money supply is the more useful liquidity measure.

Since March 2020, both global money supply and the S&P 500 have risen sharply. The stock market has risen about three times faster than the money supply over this stretch — which is almost exactly what the era-4 sensitivity (a tripling) would predict. That gap is the elasticity, not a sign of detachment.

Each asset moves on its own clock

Not every asset absorbs liquidity at the same speed. Stocks in era 4 show a real but not overwhelming connection - moving together more often than not with global money supply in the same month (about +0.36). Bonds move on that same clock too, but with a stronger, more reliable monthly connection in price terms (about +0.52).

Bitcoin looks different. At the same-month level it does not show a convincing era-4 link, but with a roughly three-month lag it does. Home prices are slower still: the strongest era-4 link shows central-bank balance sheets leading US home prices by about five months.

That is one of the most useful practical findings from the study. Liquidity matters broadly in this regime, but timing matters almost as much as direction.

Bonds may be the cleanest signal of all

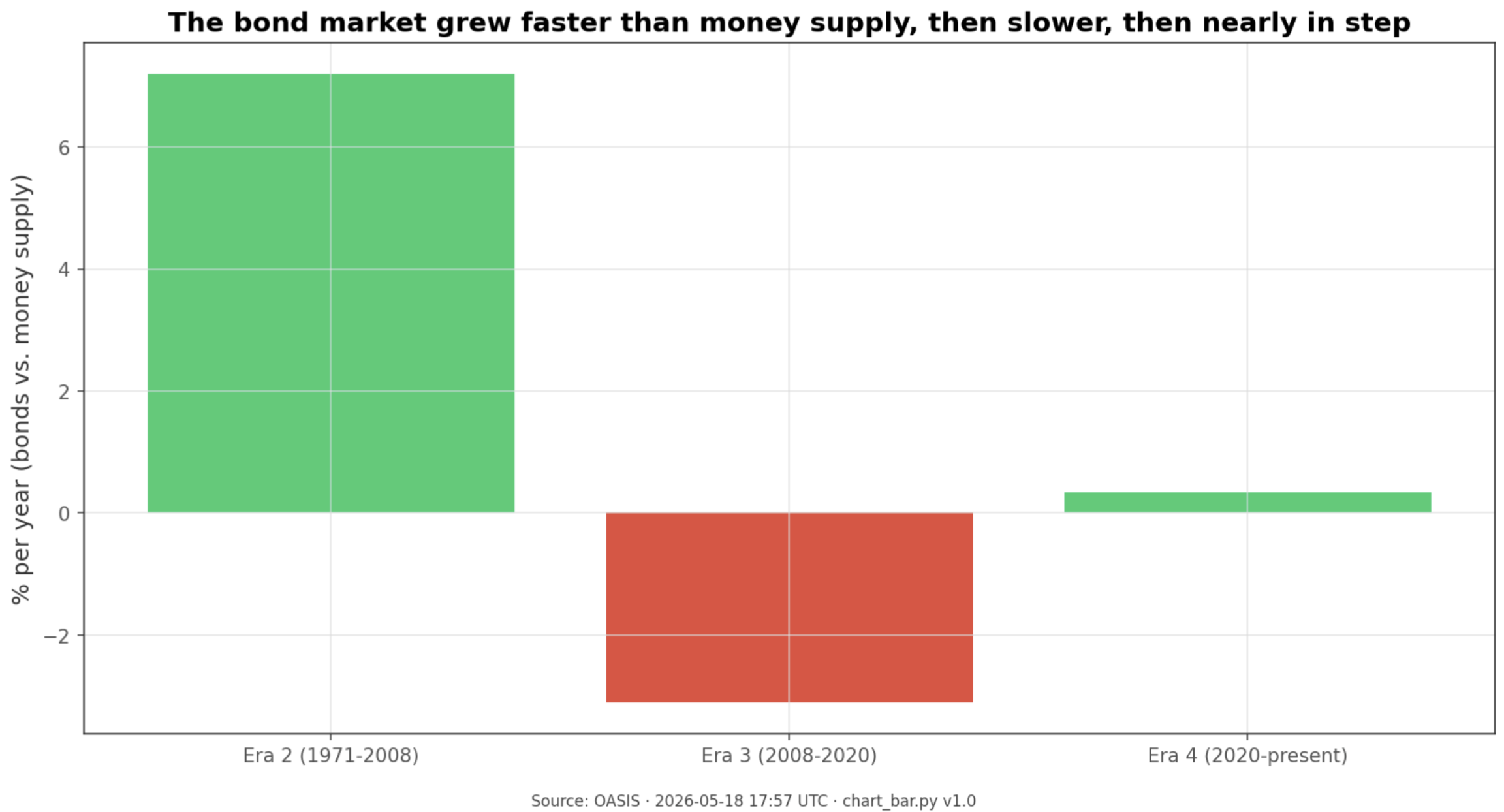

The strongest relationship in the whole matrix was not a price series at all. It was the size of the international bond market relative to global money supply. In era 4, bond-market size and global money supply grew almost in lockstep quarter to quarter, with a correlation of +0.888.

That pattern also carries a clean era fingerprint. In era 2, the BIS bond-market-to-global-money-supply ratio grew about +7.20% per year. In era 3, it fell about -3.10% per year. In era 4, it is growing only about +0.34% per year.

The size of the world bond market grew faster than the money supply in the 1971–2008 era, slower than the money supply during the QE years of 2008–2020, and then almost exactly in step from 2020 onward. Three completely different relationships — one for each era.

What to Watch

Whether the broad money supply keeps rising while central-bank balance sheets stay flat or keep shrinking; if it does, the era-4 decoupling between narrow and broad liquidity remains intact.

Whether new SPX highs continue to arrive alongside a rising global money supply; that would support the view that 7,408 is liquidity-supported rather than detached.

Whether the 12-month momentum in the global money supply keeps pointing to expansion or starts to cool; era 4 asset behavior has been materially different across those regimes.

Whether Bitcoin continues to respond with a delay rather than immediately after liquidity shifts; the three-month lag is the key test of the liquidity-beta story.

Whether bond-market size and the global money supply keep growing in near lockstep; a meaningful break there would be an early sign that the regime itself may be changing.

Look out for next week’s newsletter for further insight into the forces shaping today’s markets.

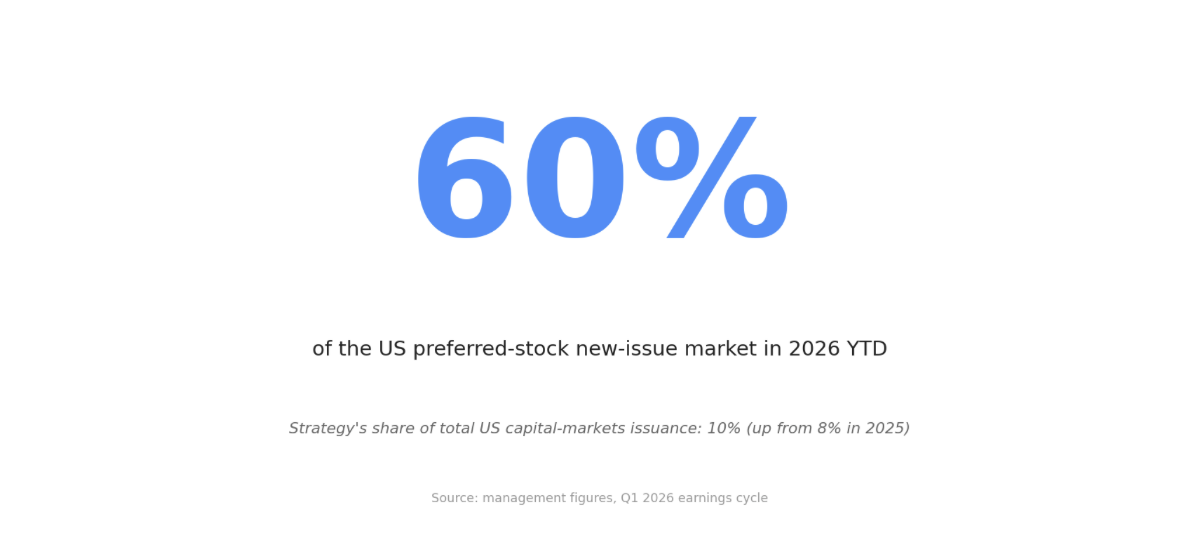

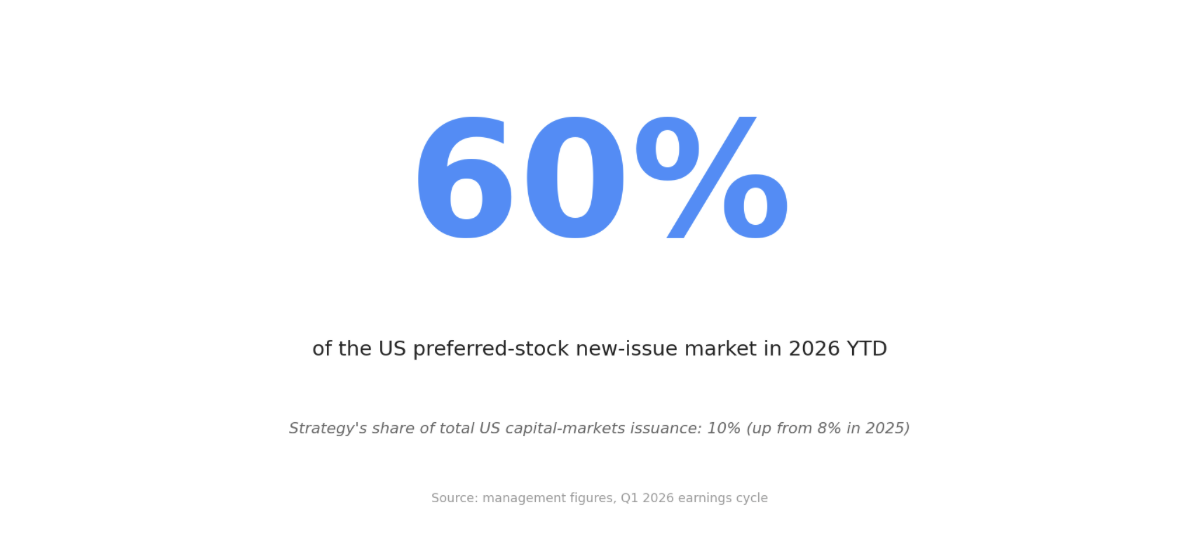

Strategy's Q1 Credit Scale-Up

Strategy's Q1 2026 cycle was less about the earnings print than about market access: $11.7B raised year to date, STRC scaled to $8.5B in nine months, and management now claims 60% of the US preferred new-issue market. The clearest evidence is the preferred side itself, with $5.6B raised YTD entirely through STRC and cumulative preferred notional at $12.13B. For readers tracking Bitcoin-linked capital formation, the point is simple: Strategy is now large enough to matter inside the preferred market, not just around its own balance sheet.

May 11th 2026

Bottom Line

Strategy's Q1 2026 cycle was less about the earnings print than about market access: $11.7B raised year to date, STRC scaled to $8.5B in nine months, and management now claims 60% of the US preferred new-issue market. The clearest evidence is the preferred side itself, with $5.6B raised YTD entirely through STRC and cumulative preferred notional at $12.13B. For readers tracking Bitcoin-linked capital formation, the point is simple: Strategy is now large enough to matter inside the preferred market, not just around its own balance sheet. Full comprehensive research report can be found below:

Thesis

This week is a single-name dispatch, and the question is straightforward: what did Strategy's Q1 2026 cycle actually advance? The answer is scale in capital markets, not a new change in corporate identity. Q1 showed that STRC is scaling fast enough to register as market structure, not just company financing.

What Changed

Last week the newsletter was about US GDP composition. This week the frame shifts to a single issuer whose funding program is now large enough to matter beyond the Bitcoin treasury story.

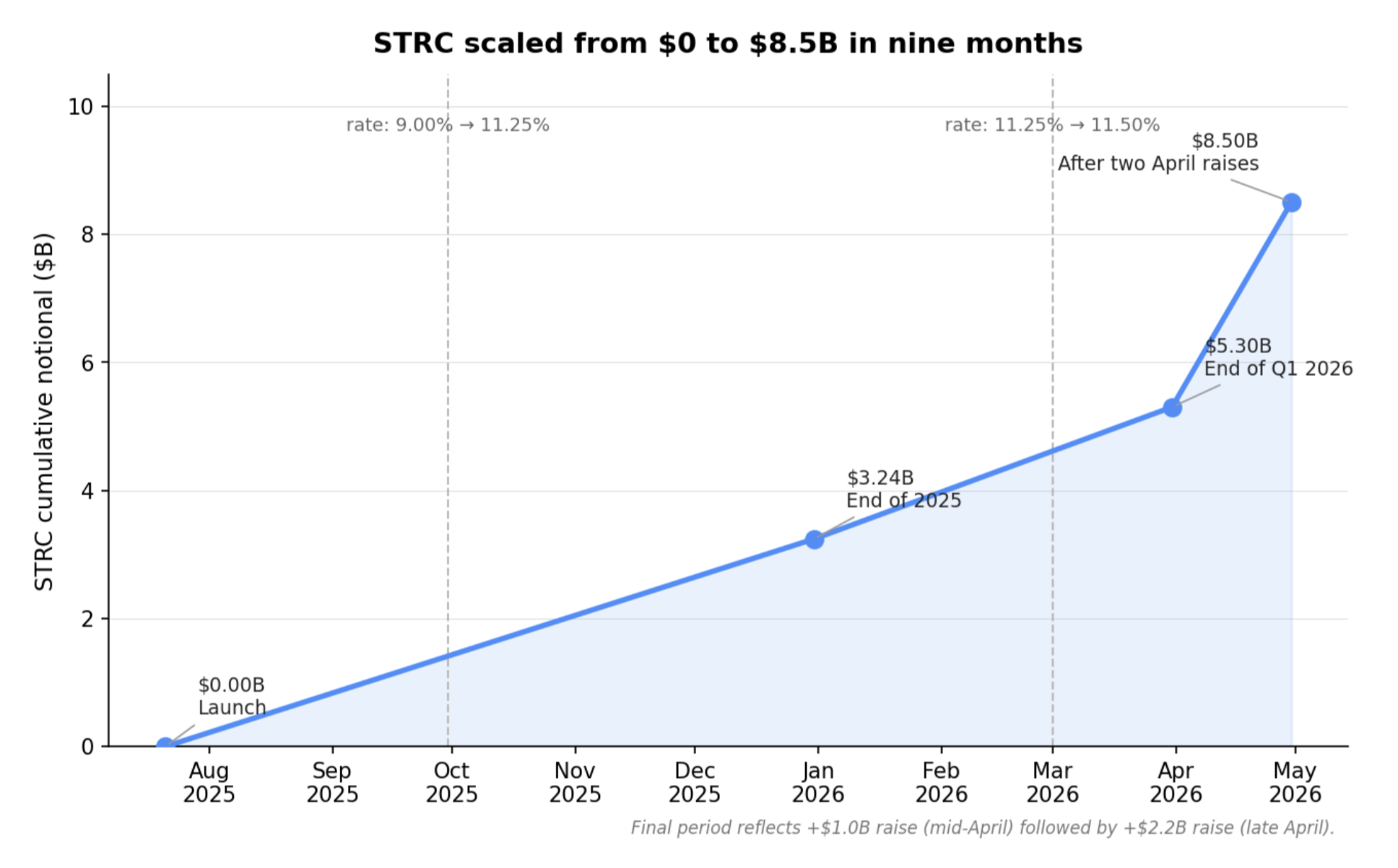

The change is scale. STRC reached $8.5B of notional in nine months, cumulative preferred equity reached $12.13B, and management says Strategy now represents 60% of the US preferred new-issue market in 2026 year to date. This week's update is that the structure kept compounding through Q1.

Evidence

The headline quarter was large, but the funding side mattered most

Strategy ended the cycle with 818,334 BTC as of May 3, equal to 3.9% of total Bitcoin supply. At the same time, the software business still generated $124.3M of Q1 revenue, up 11.9% year over year, with subscription services up 59%.

The cleaner message from the quarter was capital access, not KPI acceleration. The BTC stack kept growing, but the operating figures were more mixed than the balance-sheet scale alone suggests.

Q1 BTC Yield was 3.2%, versus 11.0% in Q1 2025.

YTD 2026 BTC Yield was 9.4%, versus 22.8% for FY2025.

BTC Gain in Q1 was 21,329 BTC, versus 49,132 a year earlier.

BTC $ Gain in Q1 was $1.45B, versus $4.05B in Q1 2025.

That mix matters for the weekly thesis because it keeps the focus on financing capacity. The quarter did add Bitcoin, but the more important development was the company's ability to keep converting investor demand into fresh balance-sheet firepower.

The quarter was really a STRC scaling story

Year to date, Strategy raised $11.7B of capital: $6.1B of common and $5.6B of preferred. On the preferred side, the issuance was effectively all STRC.

Q1 ATM net proceeds totaled $7.36B.

Of that, $5.29B came from Class A and $2.06B from STRC.

STRK contributed just $3.0M, while STRF and STRD ATMs were dormant.

Cumulatively, STRC has reached $8.5B in nine months, which management describes as the largest preferred stock by market cap in the world. Across the preferred stack, total notional is $12.13B, with STRC accounting for more than 60% of the total.

Management is still tuning the product as it scales. STRC's dividend rate was raised from 11.25% to 11.50% effective March 1, 2026, and shareholders are being asked to approve a shift from monthly to semi-monthly dividends starting in July 2026 if approved. The quarter also showed issuance flexibility: January was 88% credit and 12% common, while April flipped to 17% credit and 83% common as the Bitcoin drawdown reweighted the mix.

That issuance mix is useful because it shows management is not treating the stack as static. The common and preferred channels are being adjusted in real time, but the preferred growth engine inside that stack is clearly STRC.

The market-share figures are now too large to ignore

Management says Strategy's share of US capital-markets issuance rose from 8% in 2025 to 10% in 2026 year to date. Inside that, it claims 60% of the preferred-equity new-issue market and 6% of the common-equity market.

The microstructure signals line up with that claim. STRC daily liquidity rose from $54-120M in January to $360M in April, management says turnover is 10 times Wells Fargo preferred, and STRC is now the #2 holding in BlackRock's PFF, a $14B preferred ETF.

There is still a limit worth keeping explicit. Even the supplied work's closest candidate for a Treasury-like instrument, STRF, had a peak-to-trough drawdown of -21.76% over 37 weeks and traded at a +533 basis point spread versus the US 10-year in the November 15 reference snapshot. The stack is scaling, but it is still pricing as risk capital, not as a cash substitute.

Implications

Q1 makes the monitoring framework narrower and more concrete. Strategy now belongs on the radar as capital-markets infrastructure, especially through STRC, not just as a Bitcoin treasury story. The practical question from here is whether that preferred-market footprint holds as management works down the convert stack and keeps expanding the BTC balance.

What's in the research edition

The standing research edition goes deeper on:

The full layered capital structure: senior debt, the five preferred series, and how STRF, STRD, STRK, and STRE compare to STRC on yield, drawdown, and seniority.

Strategy's three-stage funding evolution since the 2020 Bitcoin pivot, and why management now wants to retire the convertible stack.

Management's forward guidance and the explicit rate-setting and ATM price-band rules that keep STRC clearing.

The capital-markets-disruption framing — Bitcoin as programmable capital, STRC as a credit-index inhabitant, and the comparison versus PFF, HY credit, and Treasuries.

Why STRF is the most Treasury-adjacent of the four preferreds but still not a Treasury substitute.

What to Watch

Whether STRC continues to take essentially all preferred issuance, because that remains the cleanest confirmation of the scaling story.

The shareholder vote on moving STRC from monthly to semi-monthly dividends, with first payment targeted for July 15, 2026 if approved.

Strategy's reported share of the US preferred new-issue market after Q2, since a meaningful drop from 60% would weaken the disruption claim.

STRC liquidity and its ability to stay in the stated $99-101 ATM band as additional supply comes to market.

Look out for next week’s newsletter for further insight into the forces shaping today’s markets.

Strategy Is Building a Bitcoin Credit Market

What we found in Strategy's Q1 2026 cycle is that the headline figures matter less than the structure they sit inside. Three findings stand out: STRC alone reached $8.5 billion in nine months, management says Strategy now represents 60% of the US preferred new-issue market, and STRC is already the #2 holding in BlackRock's PFF. For readers, the key implication is that Strategy now matters less as a quirky Bitcoin proxy and more as a live test of whether Bitcoin can be continuously securitized into credit and equity products that traditional markets will absorb.

Bottom Line

What we found in Strategy's Q1 2026 cycle is that the headline figures matter less than the structure they sit inside. Three findings stand out: STRC alone reached $8.5 billion in nine months, management says Strategy now represents 60% of the US preferred new-issue market, and STRC is already the #2 holding in BlackRock's PFF. For readers, the key implication is that Strategy now matters less as a quirky Bitcoin proxy and more as a live test of whether Bitcoin can be continuously securitized into credit and equity products that traditional markets will absorb.

Thesis

We approached this research by starting with Q1 and then zooming out. On the surface, the quarter offered familiar headline figures: 818,334 BTC held as of May 3, $11.7 billion raised year-to-date, software revenue of $124.3 million, and a management-reported mNAV, or market value of the total capital structure relative to Bitcoin net asset value, of 1.27x. But as we worked through the findings, what the research kept pointing back to was something more structural. Strategy is not easiest to understand as only a software company that bought a lot of Bitcoin, nor only as a leveraged equity wrapper around BTC. By management's own framing and by the shape of the issuance data, it is trying to become the securitization layer between Bitcoin and traditional capital markets. The path through that claim is straightforward: first who Strategy is today, then what the Q1 2026 earnings cycle actually said, then how those instruments are interacting with traditional markets.

Who Strategy Is Today

One company on paper, two activities in practice

We started by asking what Strategy actually is today as a company. The findings gave a clear answer: Strategy reports a single GAAP segment, but the business now clearly operates through two activities, Bitcoin treasury operations and AI-powered enterprise analytics software.

The software side is still real. FY2025 software revenue was $477.2 million, and Q1 2026 software revenue was $124.3 million, up 11.9% year over year, with subscription services up 59%. Leadership remains centered on Michael J. Saylor as Executive Chairman, Phong Le as President and CEO, Andrew Kang as CFO, and Thomas C. Chow as EVP and General Counsel.

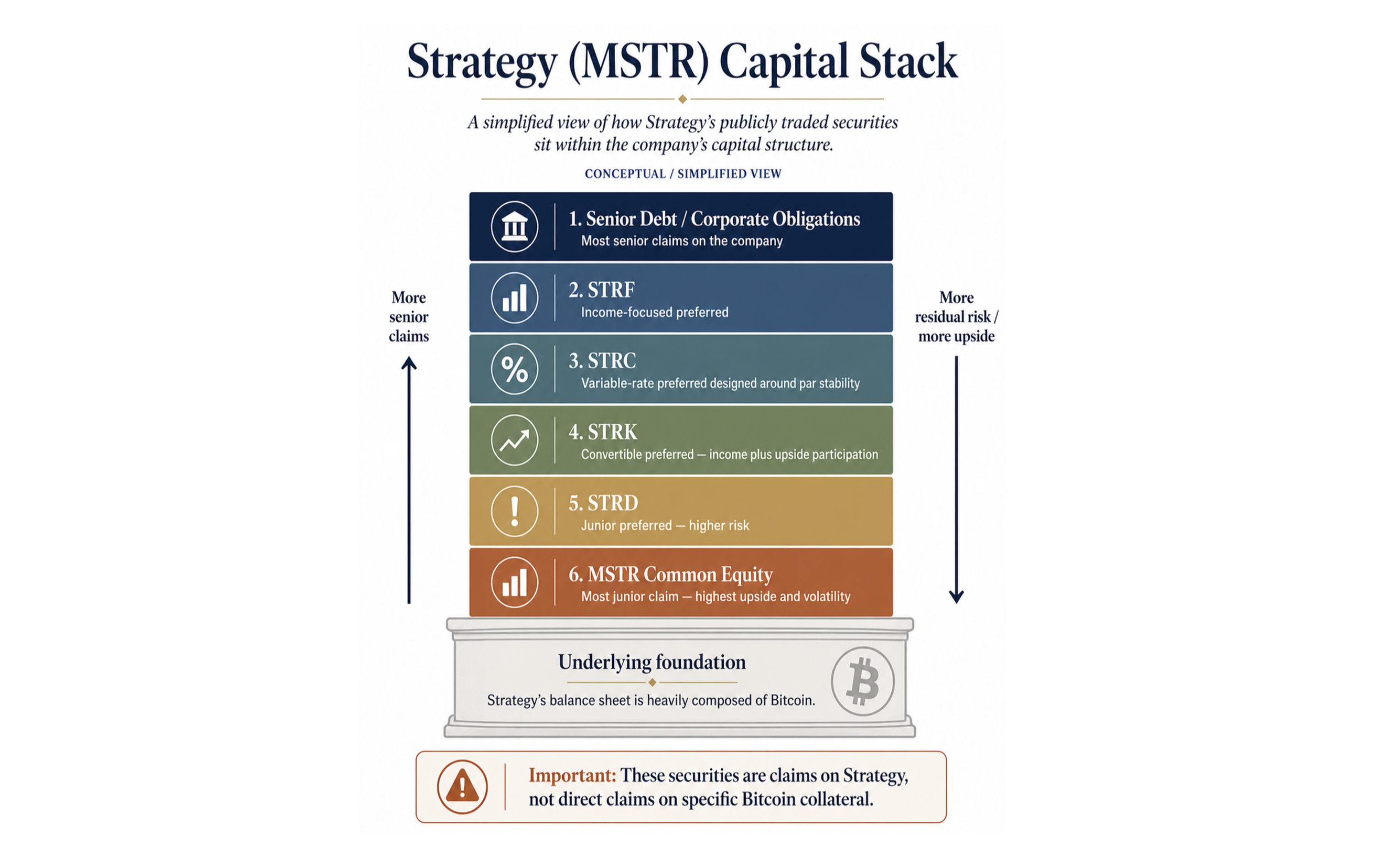

We also found that the capital structure is broader than many readers may assume. As of February 13, 2026, Strategy had 314.1 million Class A shares, 19.6 million Class B shares, and five preferred series outstanding: STRK, STRF, STRD, STRC, and STRE. That fifth series matters because it shows the preferred stack is not a side project. Strategy is still an operating software company, but the organizational shape now supports a much larger capital-markets experiment.

The pivot became the company

We then asked how the company moved from enterprise software vendor to Bitcoin treasury vehicle. What the research found is that the shift was not a one-off balance-sheet decision. It became formal company strategy.

The strategic shift began in August 2020 with the first Bitcoin purchase. In September 2020, the board adopted a Treasury Reserve Policy making BTC the primary treasury reserve asset. By Q1 2021, raising capital to accumulate Bitcoin had become formal corporate strategy.

From there, the funding mix evolved in three stages. From roughly 2020 through 2023, Strategy relied on ATM, or at-the-market, common issuance, senior convertibles, and a collateralized term loan. In 2024, scale stepped up with $16.33 billion of Class A ATM proceeds plus multiple convertible offerings. In 2025, the architecture changed again: five preferred series were issued alongside 2030B converts and another $13.59 billion of Class A ATM proceeds.

The shift across instruments is easier to see in the picture below.

That sequence matters because, in our findings, it reads as intent rather than improvisation. By the FY2025 10-K, management described Strategy as a Bitcoin Treasury Company that "structures and securitizes Bitcoin." The software business is still there, but it is no longer the strategic frame. It now looks more like operating ballast beneath a balance sheet designed to manufacture investable BTC-linked instruments.

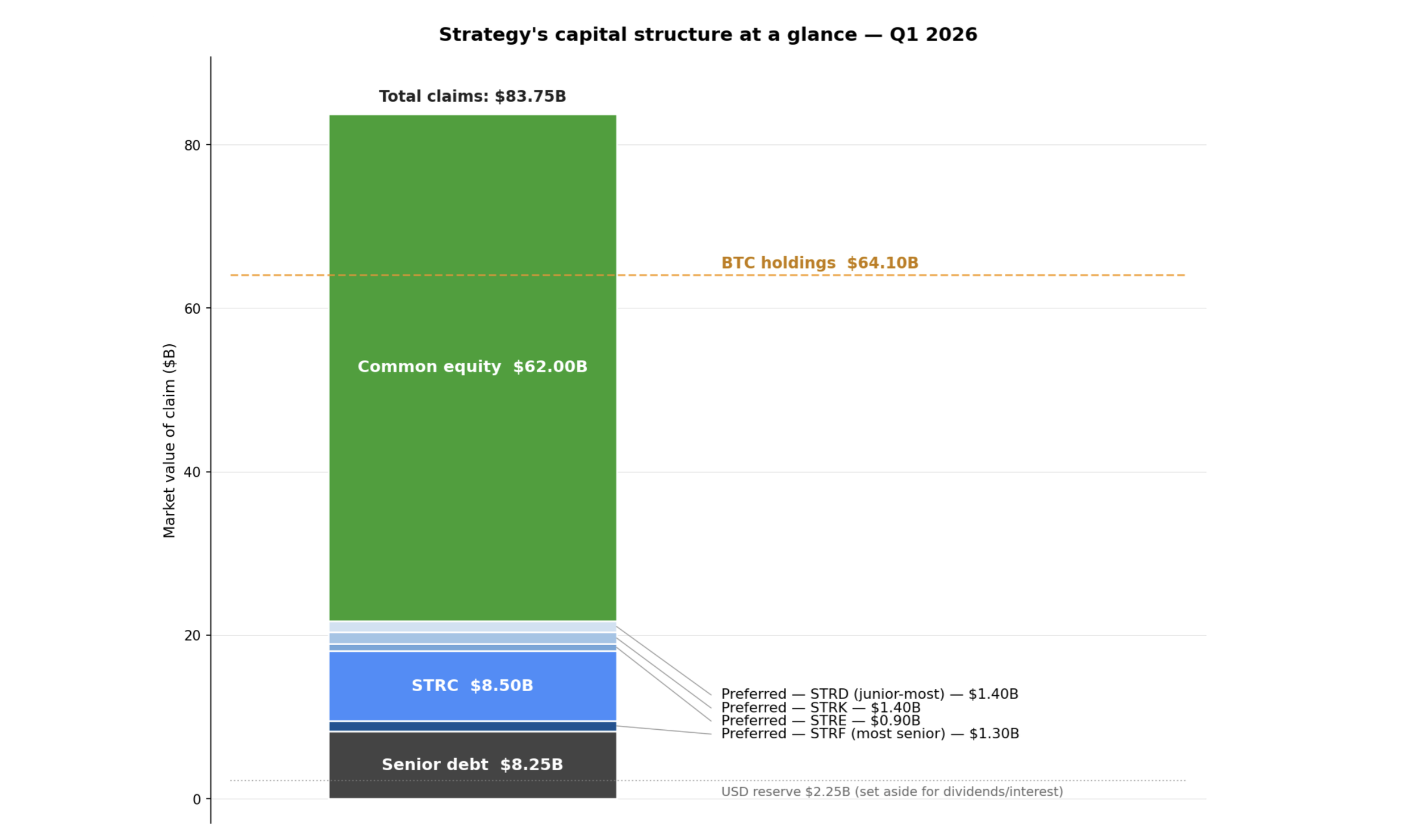

A capital stack that is large, layered, and moving away from converts

Once the strategic pivot was clear, we asked what the capital structure actually looks like now. The answer from the findings is that it is already large, layered, and increasingly organized around preferred equity rather than future convertible issuance.

As of March 31, 2026, Strategy had 314.1 million Class A shares and 19.6 million Class B shares, implying a common market cap of about $62 billion.

Above that common sits a sizeable preferred layer. The five preferreds total roughly $13.5 billion notional, with STRC alone at $8.5 billion, or more than 60% of the stack. There are also six convertible series due 2028-2032 with 0.625% to 2.25% coupons totaling $8.21 billion principal, plus $40.3 million of other long-term debt. Total indebtedness was $8.25 billion, and that debt sits senior to all preferreds, meaning the preferreds rank behind in payment priority if Strategy ever had to pay creditors out.

The chart below shows the layers to scale.

Against that sits the Bitcoin position: 818,334 BTC as of May 3, equal to 3.9% of total BTC supply and worth $64.1 billion at the cited market price, plus a dedicated USD reserve of $2.25 billion for preferred dividends and interest. We also found that management wants to equitize the convert stack over time and avoid new converts. The destination is not more debt complexity. It is common, preferred, BTC, and a cash reserve.

What the Q1 2026 Earnings Cycle Showed

Headline figures: continuity, with the machine still running

With that structure in view, we asked what Q1 itself actually showed. At the surface level, the findings looked familiar: more BTC, more capital raised, and another set of management KPIs.

Strategy reported 818,334 BTC as of May 3, worth $64.1 billion at $78,374 per BTC, with a cost basis of $61.81 billion and an average cost of $75,537.

The quarter's internally promoted performance metrics were softer than the prior comparison period. Q1 BTC Yield, the rate at which Strategy is growing Bitcoin per share, was 3.2% versus 11.0% in Q1 2025. Year-to-date 2026 BTC Yield was 9.4% versus 22.8% for FY2025. Bitcoin per share, measured against an expanded share count that includes preferreds and convertible bonds, still rose, but more slowly than a year earlier. BTC Gain was 21,329 BTC in Q1 versus 49,132 a year earlier, and BTC $ Gain was $1.45 billion versus $4.05 billion.

At the same time, the operating business remained visible. Software revenue was $124.3 million, up 11.9% year over year, with subscription revenue up 59% and gross profit at $83.4 million. Capital raised year-to-date reached $11.7 billion, split between $6.1 billion common and $5.6 billion preferred. The quarter did not change the story so much as confirm how large the machine has already become.

STRC dominated the quarter

When we asked what defined the quarter, the answer kept coming back to one instrument: STRC. The findings were decisive on that point.

Q1 2026 was decisively STRC-dominated: STRC ATM issuance raised $2.06 billion through 20.66 million shares, while Class A ATM raised $5.29 billion and STRK ATM was only $3 million. STRF and STRD ATMs were dormant.

Cumulatively, STRC reached $8.5 billion in just nine months. Management says that makes it the largest preferred stock by market cap in the world. The growth curve makes the pace clear.

The issuance mix also shifted sharply inside the quarter. In January, ATM activity was 88% credit and 12% MSTR common. By April, it had flipped to 17% credit and 83% MSTR common as the Bitcoin drawdown reweighted issuance.

Two April weeks still stand out in the findings: one $1.0 billion raise followed by a $2.2 billion raise the next week. STRC's dividend rate was also raised from 11.25% to 11.50% effective March 1, 2026. That combination of scale, active rate-setting, and sustained issuance is what makes STRC worth attention. It is no longer a concept product. It is functioning as a primary funding channel.

The dividend-frequency proposal is product iteration, not plumbing

We also wanted to know whether the proposed shareholder vote on STRC's dividend schedule was cosmetic or meaningful. The research pointed to the second reading: this looks more like product iteration than routine plumbing.

Strategy wants to move STRC from 12 dividend payments a year to 24, starting in July 2026 if approved.

The economics do not change. The proposal changes payment frequency from monthly to semi-monthly, with the first record date on June 30, 2026 and the first payment date on July 15, 2026. Management's stated reason is direct: improve attractiveness, enhance liquidity, and support better price stability.

That matters because, in the findings, STRC is being managed as an instrument whose market behavior can be tuned. The company is not simply issuing preferred stock and accepting whatever secondary-market profile follows. It is actively adjusting the user experience of the security in order to deepen demand and stabilize the channel. In that sense, the dividend-frequency proposal belongs in the same family as the coupon adjustments and price-band management. It is another signal that Strategy is iterating a market product, not merely maintaining a funding line.

Forward guidance reads like a balance-sheet blueprint

We then asked what management's forward guidance was really describing. The answer from the research is that it reads less like ordinary guidance and more like a blueprint for how the balance sheet is meant to scale.

Saylor's headline statement was the clearest version: Strategy expects to pass 1 million Bitcoin on the balance sheet within the next 36 months while funding all obligations with Bitcoin.

That sits inside a broader set of commitments. Management laid out a goal to double Bitcoin Per Share in seven years under a scenario assuming 16% Digital Credit issuance, a 9% dividend rate, and 1.75x mNAV. It also outlined six capital-markets principles: increase Bitcoin per share; grow STRC demand; reduce convertible debt proactively; size the USD reserve to credit demand and risk; adjust issuance scale to market conditions; and remain willing to sell BTC when advantageous.

The operating rule set for STRC was equally specific. If monthly average traded price falls below $95, management would recommend at least a 0.50 percentage-point rate increase; between $95 and $99, at least 0.25 percentage points; above $101, a rate decrease and/or follow-on offering. The message from the findings is straightforward: this is not passive treasury management. It is active balance-sheet engineering.

The macro framing was capital-markets disruption, not a Fed call

We also asked how management chose to frame the quarter. The findings here were notable because the central story was not the usual monetary-policy discussion. It was capital-markets disruption.

Strategy's own language was that it transforms "Digital Capital into Digital Credit and Equity," positioning itself as the securitization layer between a $1.6 trillion Bitcoin market cap and traditional preferred or fixed-income buyers.

Three threads carried that framing. First, Bitcoin was presented as programmable capital. Second, STRC was presented as a credit-index inhabitant, with Saylor stating that "Stretch is the #2 holding in BlackRock's PFF," the $14 billion preferred ETF. Third, management argued Bitcoin's risk-and-return profile can be split into a high-yield, lower-volatility credit product, STRC, and a higher-volatility equity product, MSTR common.

Phong Le also made the near-term demand point explicit: demand is more constrained by awareness and market development than by Fed moves. The quarter was therefore less a monetary-policy commentary than a product-distribution commentary.

In the Q&A, management treats the stack as a dynamic machine

Finally, we looked at what the analysts were actually asking and how management answered. That part of the research reinforced the same thread: management appears to treat the stack as a dynamic machine rather than a set of separate financing buckets.

Eight named analysts focused on five broad themes: proactive capital-stack management, the effect of lower rates, decentralized finance, or DeFi, products built on STRC, decentralization concerns as institutions accumulate BTC, and what lower BTC volatility would do to the model.

Across those answers, management's thread was consistent. It is willing to sell BTC for tax or optimization reasons, retire all convertible bonds, which can convert into shares under set conditions, via STRC, equity, or cash, and lean further into the use of leverage if BTC volatility falls. On the DeFi question, management said yield coins and leveraged yield products are already being built on STRC. On the relative-risk debate, Saylor said the market "does not yet agree."

That matters because it reveals the mindset behind the structure. Management does not appear to view the preferreds, converts, common ATM, and BTC position as separate financing buckets. It views them as coordinated levers. The quarter's educational value is not just in the numbers reported, but in how openly the company described the operating logic of the machine.

Where These Instruments Sit in Traditional Markets

Demand is strongest in STRC, but the spreads still say credit risk

Once the quarter's internal logic was clear, we asked how these instruments compare with traditional markets. The first answer was that demand is strongest in STRC, but the pricing still says credit risk rather than something Treasury-like.

The clearest demand signal is STRC: year-to-date 2026, all $5.6 billion of preferred ATM issuance came through that one series. Retail ownership is roughly 80%, and daily liquidity rose from $54-120 million in January to $360 million in April. Management says STRC turnover is 10 times that of Wells Fargo preferred.

The cross-section also matters. STRK carries an 8.00% fixed coupon, has returned -7.79%, and saw a -41.98% max drawdown. STRF carries a 10.00% fixed coupon, returned +23.18%, and had a -21.76% drawdown. STRD carries a 10.00% fixed coupon, returned +2.92%, and had a -29.09% drawdown. STRC, now at an 11.50% variable rate, returned +22.52% with only a -4.02% max drawdown.

But the yield and spread comparisons keep the framing honest. Versus PFF's typical roughly 6% distribution yield, MSTR preferreds run about 4 to 7 percentage points wider. Versus today's 2.79 percentage-point spread over Treasuries for high-yield corporate credit, they price 2 to 4 times wider than high-yield corporate credit.

STRF looks Treasury-adjacent but is not a Treasury substitute

We wanted to see whether any of the preferreds behaves like a Treasury substitute. STRF was the closest candidate, and the answer turned out to be subtler than we expected.

Within the preferred stack, it is the most senior preferred, cumulative, meaning missed dividends accrue and must be paid before common dividends resume, fixed at a 10.00% coupon, has no conversion feature, and no ordinary call. It also trades closest to par, at $100.55 latest and $105.58 on November 10, and delivered the best realized total return of the four at +23.18%.

The limits are just as important. STRF's peak-to-trough drawdown was -21.76% over 37 weeks, which is not compatible with literal "no-risk" language. Its spread versus the US 10-year at the November 15 anchor was +5.33 percentage points, firmly in high-yield-credit territory by spread. And structurally, it is subordinated to $8.25 billion of senior debt plus all subsidiary liabilities.

The right comparison from the findings is therefore not Treasury substitute. It is "treasury-spread fixed-coupon perpetual." That sounds like a narrower distinction than it is. STRF may be the most bond-like product in the stack, but the evidence still places it much closer to long-duration high-yield risk than to Treasury cash-equivalent behavior.

Strategy is already large enough to matter in the markets it touches

We then asked whether Strategy is actually large enough to influence the markets it touches, or whether the disruption framing is still mostly rhetorical. The research came back with a fairly clear answer: by management's own market-share figures and by the market-microstructure signals, it is already large enough to matter.

By management's figures, Strategy's share of US capital-markets issuance rose from 8% in 2025 to 10% in 2026 year-to-date.

Inside that, the preferred-equity figure is the eye-catching one: 60% of the US preferred new-issue market, alongside 6% of common-equity issuance. Since the Bitcoin pivot, cumulative issuance is estimated at $81.75 billion. The headline figure is the one worth keeping in mind.

The market-microstructure evidence lines up with the issuance share. STRC daily liquidity rose from $54-120 million in January to $360 million in April, and management says turnover is 10 times that of Wells Fargo preferred. STRC is also said to be the #2 holding in BlackRock's PFF.

The direct-pricing signal remains the cleanest expression of that influence. STRC has held its $99-101 trading band 100% of the time since the ATM was anchored there, and management raised the coupon from 9.00% to 11.25% to 11.50% instead of letting the price slip during BTC drawdowns. The broader preferred-market impact is not fully verified, but the instrument-level influence is already material.

Implications

The research points to a simple but important conclusion: Strategy deserves attention now less because it owns a lot of Bitcoin and more because it is testing whether Bitcoin can support an enduring securitization layer across common equity, preferred equity, and eventually a simplified post-convert capital stack. For readers tracking capital markets, the relevant signal is not just BTC sensitivity. It is product acceptance. STRC's scale, liquidity growth, ETF penetration, and price-band mechanics suggest that at least one instrument has already crossed from concept into functioning market object. At the same time, the spreads, drawdowns, subordination, and the company's tax framing for preferred dividends suggest caution in how the products are interpreted. This is a live capital-markets innovation, not a cash-equivalent revolution. The interesting question the research leaves us with is not whether the products exist. It is whether demand remains durable enough for the issuance machine to keep compounding without a major break in the stack's risk pricing.

What to Watch

What the findings suggest is worth watching next is straightforward:

Whether STRC continues to hold the $99-101 trading band after the proposed move to semi-monthly dividends; that is the cleanest test of whether the product-design tweaks are still improving liquidity and price stability.

Whether preferred issuance remains concentrated in STRC or broadens again to STRF, STRD, or STRK; Q1's $5.6 billion preferred ATM being entirely STRC is a strong but narrow demand signal.

Whether management actually reduces the $8.21 billion convertible stack over coming quarters; the stated destination is common plus preferred plus USD reserve, so convert retirement is the key execution test.

Whether STRC retains meaningful benchmark-style demand, especially its stated position as the #2 holding in BlackRock's PFF; sustained ETF and retail absorption matters more than one quarter of issuance volume.

Whether BTC accumulation keeps tracking the stated 1 million BTC in 36 months goal without forcing a visible deterioration in pricing across the preferred stack, particularly given STRF's high-yield-like spread profile and the broader subordination beneath $8.25 billion of senior debt.

Look out for next week’s newsletter for further insight into the forces shaping today’s markets.

The Shape of the US Economy

A look through the latest GDP release shows a country powered by consumption, built around services, and still being reshaped by post-2000 and post-COVID shifts.

May 4th 2026

A look through the latest GDP release shows a country powered by consumption, built around services, and still being reshaped by post-2000 and post-COVID shifts.

Bottom Line

The 2025-Q4 GDP snapshot shows a US economy led by household consumption on the spending side and by services on the production side. Personal consumption expenditures, or PCE, account for 68.0% of nominal GDP, while Finance, Insurance, and Real Estate is the largest production supersector at 21.1%. The deeper story is that government's real share has been shrinking for years, distribution has climbed the economic rankings, and several post-COVID shifts now look durable enough to treat as part of the current structure.

High Level

The cleanest high-level view of the US economy starts with two ranked lists from 2025-Q4. The first shows how output is spent: by households, businesses, government, or through trade with the rest of the world. The second shows where output is produced: which sectors make up the economy underneath those spending flows. Read together, they show a country centered on consumption, dominated by services, supported by a notably large real-estate footprint, and shaped by structural changes that began well before 2026 but remain visible in the latest data.

Evidence

1) The spending ranking starts with the consumer

The expenditure breakdown is straightforward. In 2025-Q4, personal consumption expenditures, or PCE - the dollars households spend on goods and services - were 68.0% of nominal GDP. Gross private domestic investment, or GPDI, was 17.5%, government consumption expenditures and gross investment, or GCE, was 17.0%, and net exports were -2.5%

| Rank | GDP expenditure component | 2025‑Q4 nominal shareShare | 2025‑Q4 nominal value ($B)Value ($B) |

|---|---|---|---|

| 1 | Personal Consumption Expenditures | 68.0% | 21,363.4 |

| 2 | Gross Private Domestic Investment | 17.5% | 5,500.6 |

| 3 | Government Consumption Expenditures & Gross Investment | 17.0% | 5,343.5 |

| 4 | Net Exports | ‑2.5% | ‑785.0 |

That is the modern US economy in one table: consumption first, investment and government well behind it, and trade subtracting from total output because imports exceed exports. The historical work shows this is not a one-quarter quirk. PCE's real share stepped up from 62.95% to 67.41% after 2000, while GCE fell from 25.37% in 1975-1993 to 20.93% in 1994-2012 and then 17.38% in 2013-2025. Net exports also shifted lower, moving from -0.72% to -3.22% after 1999.

One accounting point matters here. GCE captures what government directly buys and invests in; it does not include transfer payments such as Social Security. Those transfers still matter economically, but they usually appear in GDP only when households spend that income, which then shows up through PCE. That is why the direct government line can shrink even while government remains economically important.

2) The production ranking shows how service-heavy the economy has become

If the spending side shows who drives demand, the production side shows what kind of economy meets it.

| Rank | Supersector | 2025‑Q4 nominal share |

|---|---|---|

| 1 | FIRE (Finance, Insurance, Real Estate) | 21.1% |

| 2 | Distribution & Hospitality | 18.5% |

| 3 | Education, Health, Social, Arts, Other (PUBSVC) | 14.8% |

| 4 | Professional & Business Services | 12.7% |

| 5 | Government | 10.7% |

| 6 | Manufacturing | 9.1% |

| 7 | Information & Communication | 5.4% |

| 8 | Construction | 4.1% |

| 9 | Utilities | 1.5% |

| 10 | Mining | 1.1% |

| 11 | Agriculture | 0.8% |

The immediate point is scale. Finance, Insurance, and Real Estate sits at 21.1%, making it the largest supersector in the economy. Distribution and Hospitality follows at 18.5%, then the broad education-health-social-services grouping at 14.8%, and Professional and Business Services at 12.7%.

All five goods-producing supersectors combined - Manufacturing, Construction, Mining, Agriculture, and Utilities - are only about 16.6% of nominal value-added. Manufacturing still matters, but it does not dominate the map. Agriculture is especially striking: at 0.8% of GDP, it holds an outsized place in the national imagination relative to its direct footprint.

Inside the production picture, real estate is one of the central structural features of the economy and worth tracking as such. More broadly, the ranking shows an economy layered through services rather than anchored in one old industrial core.

3) Government's shrinking share is real, but it is mostly a state and local story

That service-heavy structure makes the government trend easier to place. Government remains large in dollar terms, but its real share has been falling for years.

On the production side, the government supersector moved from 16.90% in 1997-2004 to 14.41% in 2005-2014 and then 11.08% in 2015-2025. On the expenditure side, GCE followed the same broad direction: 25.37% in 1975-1993, 20.93% in 1994-2012, and 17.38% in 2013-2025.

The more interesting finding is where that decline comes from. At the industry level, state and local government fell from 9.95% in 2005-Q2 through 2013-Q2, to 8.70% in 2013-Q3 through 2020-Q2, to 7.64% in 2020-Q3 through 2025-Q4. Federal government also declined, but less sharply, moving from 4.39% to 3.92% to 3.52%. State and local government fell 2.31 percentage points; federal government fell 0.87 percentage points.

So "government is shrinking as a share of the economy" is true, but incomplete. Most of the contraction comes through the state and local line, not the federal one.

4) Distribution and several post-COVID shifts now look structural

If government's share moved down, other parts of the economy moved up. One clear example is Distribution and Hospitality.

Distribution and Hospitality now accounts for 18.5% of nominal GDP. The structural-shift work found two clean break-points: 14.78% in 1997-2011, 17.43% in 2012-2020, and 20.29% in 2021-2025. That is a combined rise of about 5.5 percentage points. The research reads the 2012 break as consistent with the e-commerce era becoming large enough to register at the supersector level, and the 2021 break as consistent with the post-COVID logistics landscape.

Implications

Taken together, the two rankings describe an economy with a clear center of gravity. Demand still runs through the household sector. Production is overwhelmingly services-led, with real estate occupying a notably large place in the structure and goods production taking a smaller share than many older mental models assume. Government's direct real share has been trending lower, mostly through state and local government, while distribution has gained share in a way that lines up with e-commerce and post-COVID logistics. The result is a more precise portrait of the US economy at the end of 2025: consumption-heavy, services-dominated, and still being reshaped by regime changes that now look well established.

What to Watch

Whether PCE stays near its current share of GDP; if consumption gives up meaningful share, the basic map changes with it.